Investment · Healthcare & Pharma

Pharma M&A Investing 2026: 5 Powerful Lessons From Eli Lilly’s $7 Billion Kelonia Deal

Eli Lilly just announced a deal to acquire Kelonia Therapeutics for up to $7 billion — $3.25 billion upfront in cash, plus up to $3.75 billion in milestone payments. It’s one of the biggest bets on next-generation cancer therapy in 2026. For young investors trying to understand pharma m&a investing, this deal is a masterclass in how Big Pharma thinks about risk, growth, and the future of oncology. Here’s what it means and the 5 lessons you need.

$7B Deal Structure

Lilly will pay $3.25B upfront plus up to $3.75B in milestone payments tied to clinical, regulatory, and commercial achievements. The structure caps downside while preserving upside — a classic pharma M&A template.

In Vivo CAR-T Bet

Kelonia’s iGPS® platform delivers genetic changes directly inside the patient, eliminating the need for chemotherapy prep used in traditional CAR-T. If it works, this could revolutionize cancer treatment economics.

Diversification Play

Lilly’s market cap sits at $887B, largely built on GLP-1 blockbusters (Mounjaro, Zepbound). This acquisition is part of a deliberate strategy to reduce revenue concentration risk before the GLP-1 boom matures.

1. The Deal: What Lilly Just Announced About Kelonia

On April 20, 2026, Eli Lilly and Kelonia Therapeutics announced a definitive agreement for Lilly to acquire the Boston-based clinical-stage biotech. The deal structure is fascinating for any investor learning how pharma M&A actually works:

| Component | Amount | When Paid |

|---|---|---|

| Upfront Cash Payment | $3.25 billion | At closing (H2 2026) |

| Clinical Milestones | Portion of remaining $3.75B | If Phase 2/3 succeed |

| Regulatory Milestones | Portion of remaining $3.75B | If FDA approval granted |

| Commercial Milestones | Portion of remaining $3.75B | If sales targets hit |

| Maximum Total Value | $7.00 billion | Over multiple years |

This structure — called a “contingent value rights” (CVR) deal — is Big Pharma’s preferred way of buying clinical-stage biotechs. Here’s why it matters: the buyer only pays the full price if the acquired company’s drug actually works. If Kelonia’s lead program fails in Phase 2, Lilly’s total outlay is capped at $3.25 billion. If it becomes a commercial blockbuster, Lilly happily pays the full $7 billion because the asset is worth multiples of that.

💡 Why This Structure Is Brilliant

In biotech, 90%+ of clinical-stage drugs fail before reaching market. A CVR structure forces the seller to share that risk with the buyer. Sellers get a headline number ($7B) that makes news; buyers retain downside protection on the money they actually deploy. This is why you’ll see “up to $X billion” in nearly every pharma acquisition announcement.

The deal is expected to close in the second half of 2026, subject to customary regulatory approvals. Lilly’s stock popped approximately 1.9% in pre-market trading on the announcement.

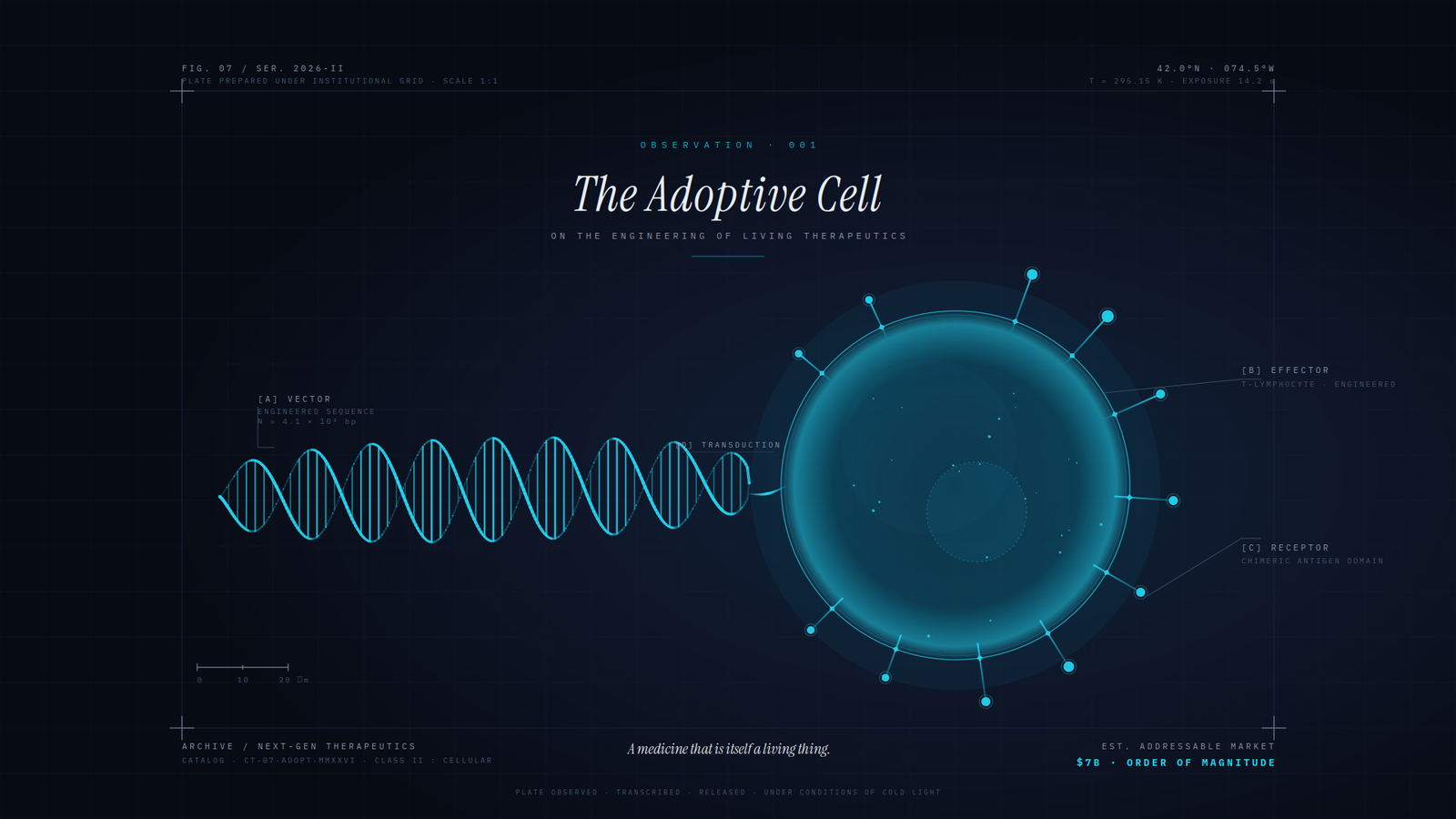

2. Why Kelonia? The Science Behind In Vivo CAR-T

To understand why Lilly was willing to pay up to $7 billion for a company that doesn’t yet have an approved product, you need to understand what Kelonia is building — and why it could disrupt a $240 billion global oncology market.

Kelonia’s lead program, KLN-1010, is an “in vivo CAR-T” therapy for relapsed/refractory multiple myeloma, currently in Phase 1 trials. The clinical data was highlighted at the 2025 ASH Annual Meeting plenary session — the biggest stage in hematology research.

Here’s what makes it potentially revolutionary:

| Feature | Traditional CAR-T | Kelonia’s In Vivo CAR-T |

|---|---|---|

| How it works | Cells extracted from patient, engineered in lab, reinfused | Engineering happens inside the patient’s body |

| Chemotherapy prep | Required (lymphodepleting chemo) | Not required |

| Manufacturing | Custom per-patient, 2-4 weeks | Off-the-shelf delivery |

| Cost per patient | $400K–$500K+ | Potentially much lower at scale |

| Accessibility | Limited to specialized centers | Broader clinical settings possible |

If KLN-1010 works and gets FDA approval, it could eliminate two of the biggest barriers to CAR-T therapy: the grueling chemotherapy patients currently must undergo before treatment, and the weeks-long custom manufacturing process. That’s the scientific thesis. The commercial thesis is even bigger: making CAR-T practical at scale could 10x the addressable patient population.

The key phrase to remember: “potentially first-in-class”. That’s biotech language for “if this works, no competitor has anything like it.” First-in-class drugs command premium pricing and market share for years before generics or biosimilars arrive.

3. The Bigger Picture: Lilly’s M&A Machine

To fully appreciate this deal, you need to understand Lilly’s overall strategic positioning. This isn’t a one-off acquisition — it’s part of a systematic program that has made Lilly one of the most active acquirers in pharma.

Since 2020, Eli Lilly has completed 16 acquisitions of mid-sized biotechs. In 2026 alone, the company has announced:

- February 2026: Orna Therapeutics for up to $2.4 billion (RNA therapies)

- Early 2026: Seamless Therapeutics collaboration for $1.12 billion (programmable recombinases for hearing loss)

- April 2026: Insilico Medicine partnership (AI-driven drug discovery)

- April 2026: Kelonia Therapeutics for up to $7 billion (in vivo CAR-T)

The strategic logic is clear. Lilly’s current valuation — $887 billion market cap at a 40.4x P/E ratio — is largely powered by its GLP-1 franchise (Mounjaro for diabetes, Zepbound for obesity). While those drugs are generating enormous cash flow right now, every pharma analyst knows the risk: blockbuster concentration. When patents expire or competitive alternatives arrive, revenue can drop sharply.

Lilly’s M&A strategy is a deliberate hedge. By aggressively acquiring next-generation assets in oncology, immunology, and gene therapy, the company is building the 2030s revenue stream before the 2020s revenue stream peaks. This is exactly how mature pharma companies extend their growth runway — and it’s one of the most important concepts in pharma investing.

As Lilly’s 2025 financial results showed, the company generated $9.4 billion in cancer medicine revenue out of $65.2 billion total revenue. That’s 14% of the pie. Kelonia could push oncology toward 20%+ of revenue by 2030 if KLN-1010 delivers. For more on how to evaluate stock valuations, see our guide on understanding P/E ratios.

4. 5 Powerful Lessons for Pharma M&A Investing

Lesson #1: The Headline Price Is Rarely the Real Price

“Lilly acquires Kelonia for up to $7 billion” is the headline. The reality is Lilly is paying $3.25 billion today, with the remaining $3.75 billion contingent on future success. In pharma m&a investing, always separate the upfront cash (what the acquirer is actually committing) from the total potential value (what the seller gets if everything goes right). The upfront is a better gauge of true deal value than the headline.

Lesson #2: Acquirers Buy “Options,” Not Just Companies

Think of biotech acquisitions like call options. Lilly is paying a $3.25B premium for the right — but not obligation — to participate in Kelonia’s upside. If KLN-1010 fails in Phase 2, Lilly walks away having spent $3.25B but avoiding another $3.75B. That’s optionality, and it’s why pharma M&A has survived even in tough economic cycles. Big Pharma is constantly buying biotech call options as part of R&D strategy.

Lesson #3: Watch What the Acquirer Is Hedging Against

When a company like Lilly — dominant in GLP-1s — aggressively acquires cancer, immunology, and gene therapy companies, they’re not doing it randomly. They’re explicitly hedging concentration risk in their current franchise. As an investor, when you see a pattern of strategic acquisitions, ask: what is management worried about? Often, the M&A program reveals management’s private concerns better than earnings calls.

Lesson #4: Clinical Stage Matters More Than Anything

Kelonia’s lead drug is in Phase 1. That means safety has been partially established but efficacy is still uncertain. The statistical odds of a Phase 1 drug reaching approval are roughly 10-15%. Lilly is paying a premium precisely because Phase 1 assets are cheap relative to their blockbuster potential if they work. As a retail investor, understand that every pharma M&A has a clinical stage that dictates both risk and valuation logic.

Lesson #5: The Picks-and-Shovels Play Often Wins

Most retail investors can’t buy Kelonia directly — it’s private. But everyone can buy Eli Lilly (LLY). And LLY’s biotech acquisition machine is a major part of its long-term value creation. In pharma m&a investing, you often capture better risk-adjusted returns by owning the acquirers (Big Pharma) rather than trying to guess which small biotechs will get bought. LLY’s current 40.4x P/E looks expensive on today’s earnings, but embedded in that multiple is the expectation that its M&A pipeline will extend growth well into the 2030s.

5. Interactive: Milestone Payment Scenario Calculator

Let’s model how much Lilly actually pays for Kelonia under different clinical outcomes. Adjust the probability sliders for each milestone stage, and see the probability-weighted expected cost of the deal. This is similar to how institutional M&A analysts evaluate these structures.

Guaranteed Upfront Payment

Paid at closing regardless of outcome

$3.25B

Expected Milestone Payments

Probability-weighted contingent value

—

Expected Total Deal Cost

What Lilly probably pays in reality

—

6. Your Pharma M&A Investing Action Plan

You probably can’t buy Kelonia Therapeutics directly — but you can use this deal as a framework for smarter pharma m&a investing decisions. Here’s the practical action plan:

- 1. Focus on the acquirers, not the targets. For most retail investors, buying LLY, MRK, PFE, or JNJ gives you diversified exposure to dozens of biotech bets without the single-asset binary risk of owning a clinical-stage biotech directly.

- 2. Read deal structures carefully. When a pharma M&A headline says “up to $X billion,” find the upfront payment. That number tells you what the acquirer is actually committing today. The contingent portion is upside that may or may not materialize.

- 3. Track the acquirer’s M&A cadence. Lilly has done 16 deals since 2020. That consistency signals a strategic discipline, not opportunistic dealmaking. Companies with steady M&A programs tend to build more durable growth than those that do occasional mega-deals.

- 4. Understand the therapeutic concentration. Lilly’s GLP-1 franchise is currently 40%+ of revenue. The oncology M&A program is specifically designed to reduce that concentration over the next 5 years. Know which “leg” of a pharma company’s revenue stool is being shored up by each acquisition.

- 5. Don’t ignore the Phase 1/2/3 distinction. A Phase 1 asset (like KLN-1010) carries 85-90% failure risk. A Phase 3 asset carries only 30-40% failure risk. When evaluating a pharma acquisition, the clinical stage dictates both the valuation logic and the realistic outcome probabilities.

Pharma is one of the most academic sectors in the market — and ironically, that makes it one of the best educational case studies for investors. Every deal has a clear thesis, a measurable risk framework, and binary outcomes that test discipline. The Kelonia acquisition isn’t just a Lilly story; it’s a textbook in how large-cap healthcare companies invest in their own future.

For more on building a resilient portfolio, read our guides on index fund investing for beginners and wealth management fundamentals.