It’s the last week of the month, and you’re staring at your bank account wondering where all your money went. You got paid two weeks ago, but somehow you’re already down to $87. You know you should have a budget, but every time you try to track every single expense in a spreadsheet, you give up after three days.

Sound familiar?

Enter the 50/30/20 rule—the budget so simple you can calculate it on a napkin. It’s been called “the only budget you’ll ever need” and “the easiest way to manage your money.” But here’s the question nobody asks: does it actually work for real people with real incomes?

The short answer: sometimes. The longer answer: it depends on where you live, how much you make, and whether you’re willing to be honest about the difference between “needs” and “wants.”

This guide will break down exactly how the 50/30/20 rule works, show you real examples at different income levels, and help you figure out if it’s right for you—or how to adjust it so it actually works with your life.

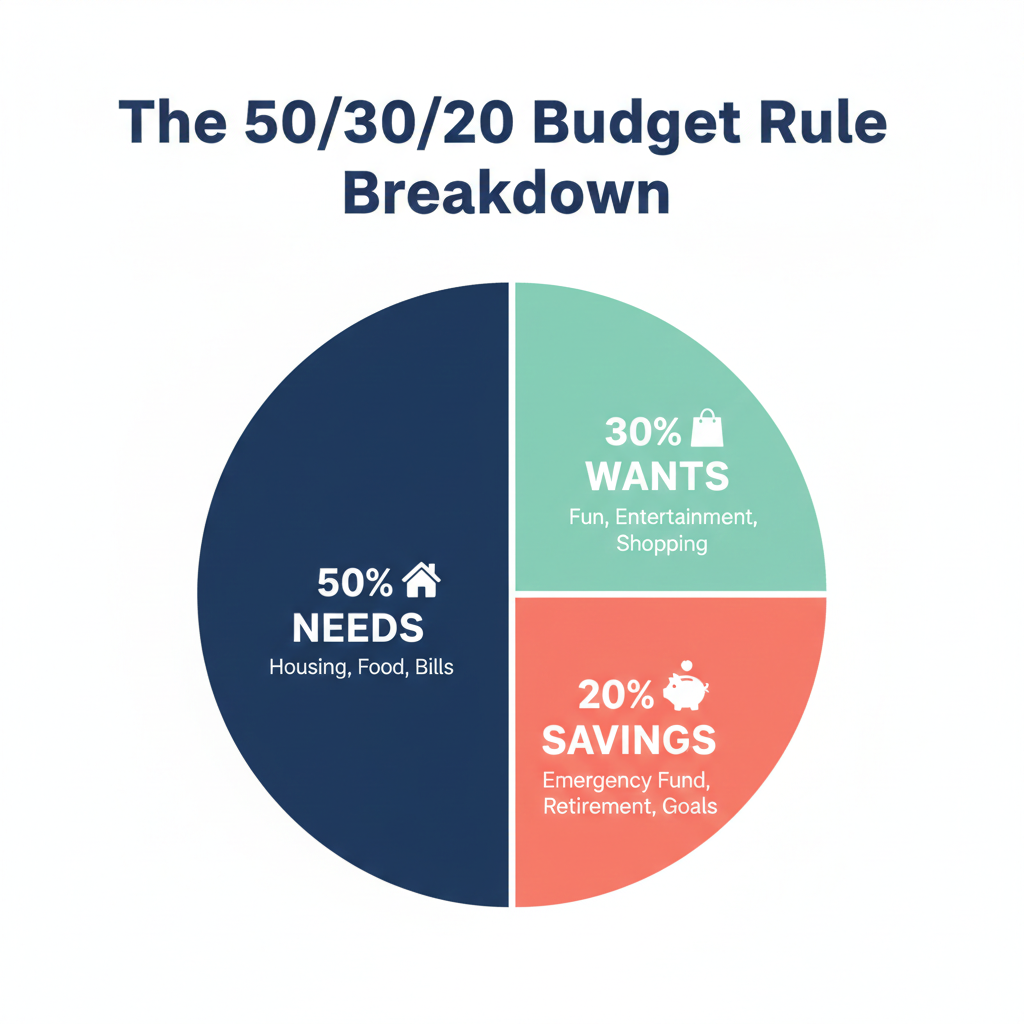

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting framework created by Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan.”[1] Here’s how it breaks down:

50% of your after-tax income goes to Needs These are expenses you genuinely can’t avoid: rent, groceries, utilities, insurance, minimum debt payments, and transportation.

30% of your after-tax income goes to Wants This is everything that makes life enjoyable but isn’t essential: dining out, streaming services, hobbies, travel, new clothes, concert tickets.

20% of your after-tax income goes to Savings and Debt Payoff This includes your emergency fund, retirement contributions, extra debt payments above minimums, and any other savings goals.

The beauty of this rule is its simplicity. You don’t need to track every coffee or categorize every transaction into 47 different budget categories. You just need to know three numbers.

Carlos, a 27-year-old teacher making $48,000 per year, tried complex budgeting apps for months. “I’d spend hours every week categorizing transactions,” he said. “Then I’d feel guilty every time I went over budget on ‘groceries’ even though I was under on ‘entertainment.’ The 50/30/20 rule gave me breathing room. As long as my needs stayed under 50% and I saved 20%, I could enjoy the other 30% without guilt.”

Breaking Down Each Category: What Actually Counts?

The tricky part isn’t the math—it’s deciding what goes in each bucket. Let’s get specific.

The 50%: Needs (Essential Expenses)

Definitely Needs:

- Housing: Rent or mortgage payment, property taxes, HOA fees

- Utilities: Electric, water, gas, internet (basic plan), phone (basic plan)

- Groceries: Food you cook at home, household essentials

- Transportation: Car payment, gas, public transit, car insurance, basic maintenance

- Insurance: Health insurance, renters/homeowners insurance, life insurance (if you have dependents)

- Minimum debt payments: Student loans, credit cards, personal loans

- Childcare: If you need it to work

The Gray Area (Be Honest):

- Internet: Basic internet is a need. Gigabit fiber so you can game? That’s a want.

- Phone: A basic phone plan is a need. The latest iPhone 15 Pro? Want.

- Car: Reliable transportation to work is a need. A $50,000 SUV? Probably a want.

The 30%: Wants (Everything Else)

Clearly Wants:

- Dining out, takeout, coffee shops

- Streaming services (Netflix, Spotify, etc.)

- Gym membership, fitness classes

- New clothes (beyond basic replacements)

- Hobbies and entertainment

- Vacations and travel

- Shopping and non-essentials

- Upgraded versions of “needs” (the fancy phone plan, the premium apartment)

Why this matters: Most people underestimate their “wants” spending. That daily $6 latte? That’s $180/month in your wants category.

The 20%: Savings and Debt Payoff

What Goes Here:

- Emergency fund contributions

- Retirement savings (401k, IRA)

- Extra debt payments (beyond minimums)

- Saving for a house down payment

- Any other financial goals (wedding, car, travel fund that you’re actually saving for)

Important: Minimum debt payments go in “needs.” Only extra payments go in the 20% category.

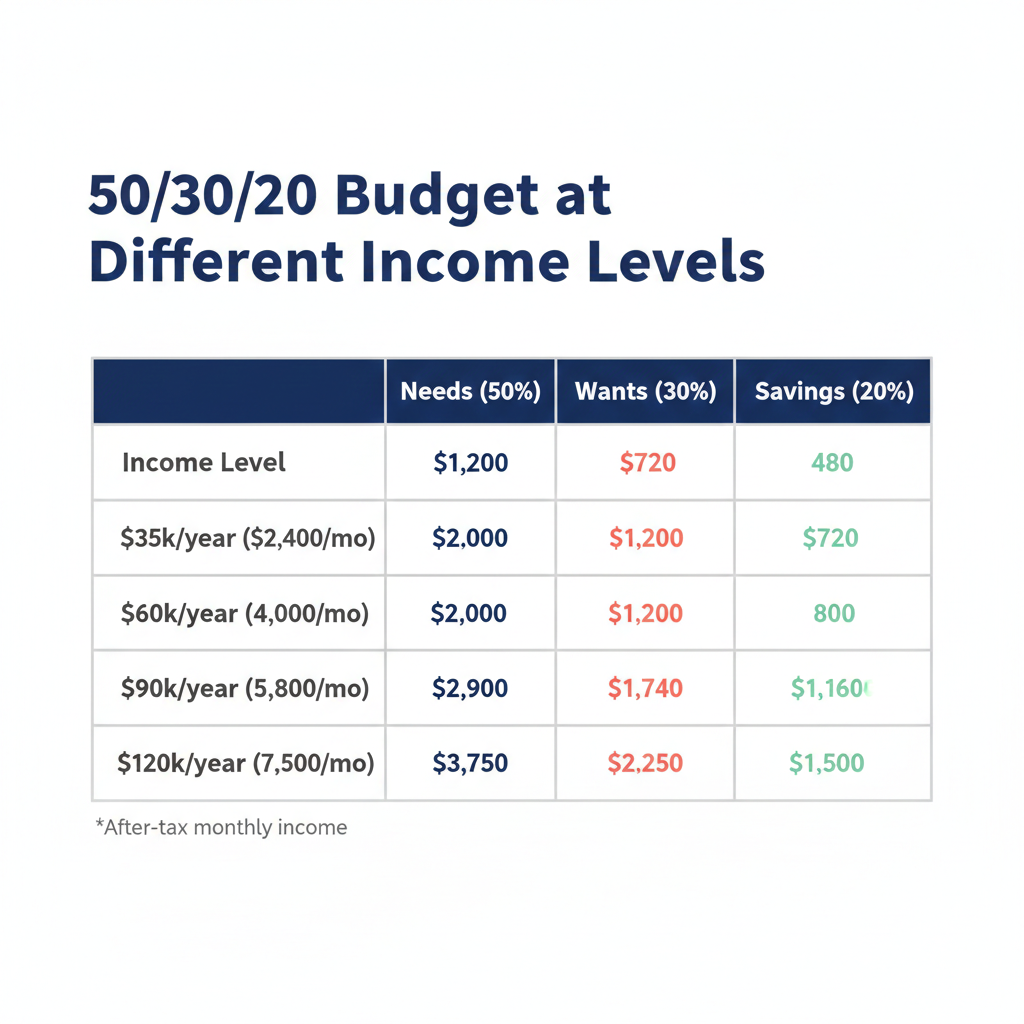

Real Examples: How 50/30/20 Looks at Different Income Levels

Let’s see how this plays out with real numbers. All examples use after-tax income.

Example 1: $35,000 Annual Income ($2,400/month after taxes)

Profile: Single, living with roommates in a mid-sized city

50% Needs ($1,200/month):

- Rent (shared): $700

- Utilities (share): $80

- Groceries: $250

- Car payment: $0 (paid off)

- Gas: $60

- Car insurance: $90

- Health insurance: $0 (employer-covered)

- Phone: $35

- Total: $1,215 (slightly over, but close)

30% Wants ($720/month):

- Dining out/takeout: $200

- Streaming services: $35

- Gym: $30

- Going out with friends: $150

- Shopping/personal: $200

- Hobbies: $100

- Total: $715

20% Savings ($480/month = $5,760/year):

- Emergency fund: $200

- 401(k): $280 (to get employer match)

- Total: $480

Does it work? Yes, but barely. There’s almost no wiggle room, and this person needs roommates to make the numbers work.

Example 2: $60,000 Annual Income ($4,000/month after taxes)

Profile: Single, renting a 1-bedroom in a mid-sized city

50% Needs ($2,000/month):

- Rent (1-bedroom): $1,200

- Utilities: $120

- Groceries: $300

- Car payment: $250

- Gas: $100

- Car insurance: $110

- Health insurance: $150 (employee portion)

- Phone: $50

- Student loan minimum: $200

- Total: $2,480 (over budget by $480!)

This is the problem. At this income level in many cities, 50% isn’t enough for true needs. Housing alone takes 30% of after-tax income, and other needs push the total to 62%.

Adjusted reality:

- Needs: 62% ($2,480)

- Wants: 18% ($720)

- Savings: 20% ($800)

Does it work? Not in the traditional 50/30/20 split. This person has to either cut wants to 18% or reduce savings—or find a cheaper apartment.

Example 3: $90,000 Annual Income ($5,800/month after taxes)

Profile: Married couple, no kids, renting in a high-cost city

50% Needs ($2,900/month):

- Rent (2-bedroom): $2,000

- Utilities: $150

- Groceries: $500

- Two car payments: $400 (total)

- Gas: $150

- Car insurance: $200

- Health insurance: $300

- Phones: $100

- Student loan minimums: $400

- Total: $4,200 (over by $1,300!)

The high-cost city problem. In cities like San Francisco, New York, or Seattle, the 50/30/20 rule falls apart completely. Housing alone eats up 34% of after-tax income.

Adjusted reality:

- Needs: 72% ($4,200)

- Wants: 10% ($580)

- Savings: 18% ($1,020)

Does it work? No. The couple either needs to move to a cheaper city, find cheaper housing, or accept a different ratio like 70/10/20.

Example 4: $120,000 Annual Income ($7,500/month after taxes)

Profile: Single professional in a high-cost city

50% Needs ($3,750/month):

- Rent (nice 1-bedroom): $2,500

- Utilities: $150

- Groceries: $400

- Car payment: $500

- Gas: $120

- Insurance: $400 (car + health + renters)

- Phone: $80

- Student loan minimum: $600

- Total: $4,750 (over by $1,000)

30% Wants ($2,250/month):

- Dining out: $600

- Travel fund: $500

- Gym/fitness: $200

- Shopping: $400

- Entertainment: $300

- Subscriptions: $100

- Hobbies: $150

- Total: $2,250

20% Savings ($1,500/month = $18,000/year):

- 401(k): $1,000

- Emergency fund: $300

- Investment account: $200

- Total: $1,500

Does it work? Better than lower incomes, but still tight in a high-cost city. This person is actually doing 63/30/20 because housing is so expensive.

When the 50/30/20 Rule Actually Works

Based on research and real-world experience, the 50/30/20 rule works best for:

People earning $50,000-100,000 in low-to-mid cost areas. If you’re making a decent income in a city where rent for a nice 1-bedroom is under $1,200, the numbers work beautifully.

People with paid-off cars. Car payments eat into the 50% fast. If you own your car outright, you free up $300-500/month.

People with employer-covered health insurance. If you’re paying $500+/month for health insurance, it blows up the “needs” category.

Dual-income households in affordable areas. Two incomes + low housing costs = the 50/30/20 rule works perfectly.

People without high-interest debt. If you’re carrying $10,000 in credit card debt, the 20% savings portion should actually go to aggressive debt payoff first.

When You Need to Adjust the Rule

The 50/30/20 rule is a guideline, not a law. Here’s when and how to modify it:

High Cost of Living Area: Try 60/20/20 or 70/10/20

If you live in San Francisco, NYC, Boston, or Seattle, you might need:

- 60-70% for needs (housing is just expensive)

- 10-20% for wants

- 20% for savings (keep this if possible)

The key is maintaining that 20% savings rate. According to Fidelity, you should be saving 15-20% of your income for retirement alone.[2]

Low Income: Try 60/20/20 or 70/10/20

When you’re earning under $40,000, your needs will likely exceed 50%. Don’t beat yourself up. Focus on:

- Covering essentials (60-70%)

- Saving anything (even 10% is better than 0%)

- Minimizing wants temporarily

High Income: Try 50/20/30

If you’re earning $150,000+, consider flipping wants and savings:

- 50% needs

- 20% wants (you don’t need 30%)

- 30% savings (accelerate wealth building)

Aggressive Debt Payoff: Try 50/20/30

If you have high-interest debt:

- 50% needs

- 20% wants (cut back temporarily)

- 30% debt demolition + savings

Pay off any debt above 8% interest before worrying about investing.

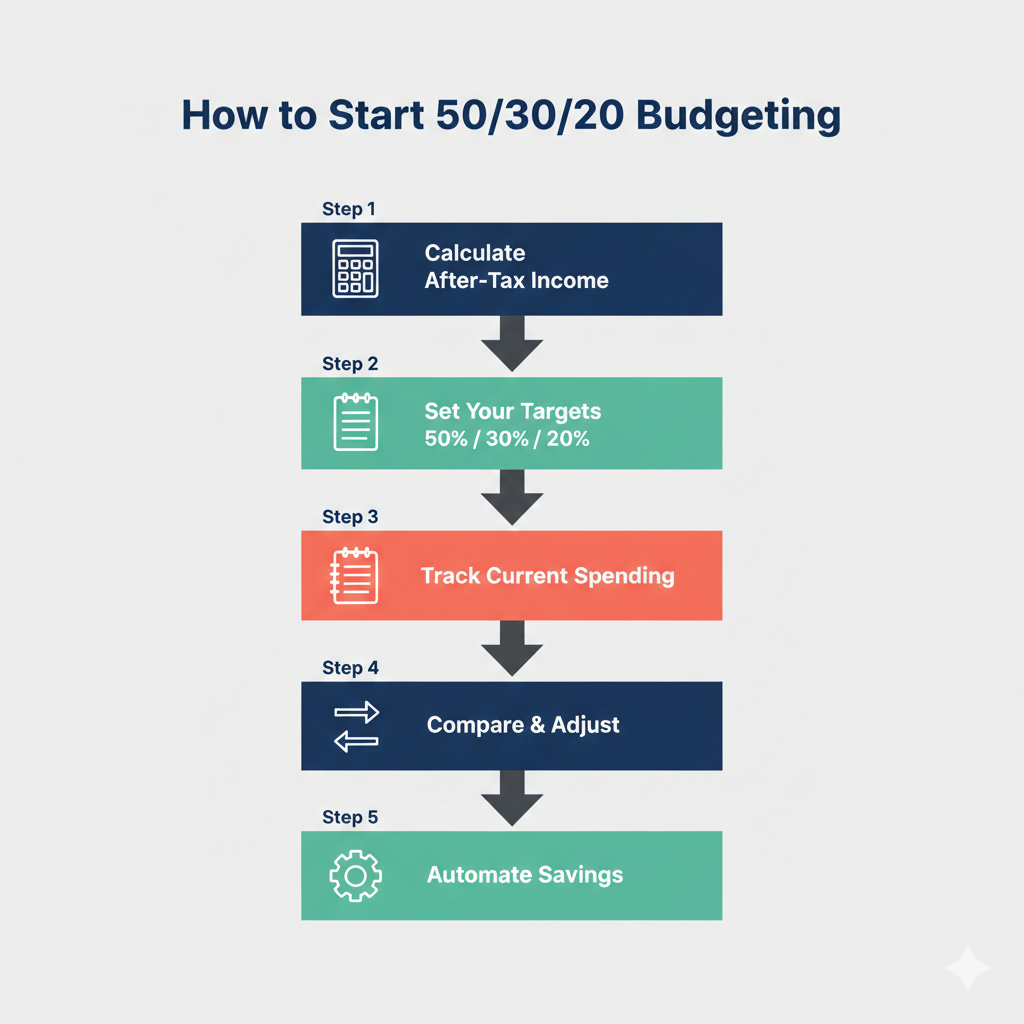

How to Actually Implement the 50/30/20 Rule

Knowing the rule is easy. Actually doing it? That takes a system.

Step 1: Calculate Your After-Tax Income

This is NOT your salary. It’s what actually hits your bank account after:

- Federal taxes

- State taxes

- Social Security and Medicare

- Health insurance premiums

- 401(k) contributions (if pre-tax)

Example: $60,000 salary might be $4,000/month after-tax.

Step 2: Calculate Your Three Numbers

- Needs budget: After-tax income × 0.50

- Wants budget: After-tax income × 0.30

- Savings budget: After-tax income × 0.20

With $4,000/month after-tax:

- Needs: $2,000

- Wants: $1,200

- Savings: $800

Step 3: Track Your Current Spending

For one month, categorize EVERY expense into needs, wants, or savings. Use:

- Bank/credit card statements

- Budgeting apps (Mint, YNAB, PocketGuard)

- A simple spreadsheet

Be brutally honest. That $70 dinner out is NOT a need.

Step 4: Compare Reality to Your Target

Most people discover:

- Their “needs” are actually 60-70% (oops)

- Their “wants” are 35-40% (double oops)

- Their “savings” are 0-5% (yikes)

Step 5: Make Adjustments

If your needs are over 50%:

- Can you find a cheaper apartment or get a roommate?

- Can you refinance your car loan or sell and buy cheaper?

- Can you shop at cheaper grocery stores?

- Can you cut your phone/internet to basic plans?

If your wants are over 30%:

- Cancel unused subscriptions

- Cook at home more (dining out is the #1 wants budget killer)

- Find free/cheap entertainment

- Implement a 24-hour rule for non-essential purchases

If you’re not saving 20%:

- Automate it first (pay yourself first)

- Start with 10% and increase by 1% every month

- Redirect any raise straight to savings

Step 6: Automate Everything

Set up automatic transfers on payday:

- Savings: Immediately move 20% to a separate savings account

- Needs: Keep in checking (these are bills anyway)

- Wants: Consider a separate “fun money” account

If the money’s already moved, you can’t accidentally spend it.

Common Mistakes People Make with 50/30/20

Mistake #1: Lying About Needs vs Wants

“But I NEED my $200/month gym membership!” No, you want it. Be honest or the budget won’t work.

Mistake #2: Forgetting Annual Expenses

Car insurance, Amazon Prime, holiday shopping—these aren’t monthly, but they’re still expenses. Divide annual costs by 12 and budget monthly.

Mistake #3: Not Adjusting for Your Reality

If you live in Manhattan, you’re not fitting rent into 50%. Adjust the rule to your life, not the other way around.

Mistake #4: Saving 20% While Carrying Credit Card Debt

If you have credit cards charging 22% interest, that 20% should go to debt first. You can’t out-invest 22% interest.

Mistake #5: Giving Up After One Month

Your first month will be messy. That’s normal. Budgets take 2-3 months to smooth out.

Budget Apps That Make 50/30/20 Easy

You don’t need fancy software, but these can help:

YNAB (You Need A Budget) – $14.99/month[3]

- Proactive budgeting

- Forces you to assign every dollar

- Great for detail-oriented people

Mint – Free

- Automatic expense tracking

- Can create 50/30/20 categories

- Good for passive tracking

PocketGuard – Free (Premium $12.99/month)

- Shows “money left to spend” after needs and savings

- Simple 50/30/20 setup

Spreadsheet – Free

- Total control and customization

- One-time setup, no monthly fees

- Best for people who like control

Pick whatever you’ll actually use consistently. The best budget app is the one you open.

Real Talk: When 50/30/20 Just Won’t Work

Let’s be honest. If you’re:

- Earning $30,000 in San Francisco

- Supporting a family on $45,000

- Drowning in debt with minimum payments eating 30% of income

- Dealing with a medical crisis

…the 50/30/20 rule might not work right now. And that’s okay.

What to do instead:

Focus on survival first: Cover your four walls (food, shelter, utilities, transportation), then work on everything else.

Emergency mode budget:

- Essential needs: 80%+

- Wants: 5%

- Savings: 5-15% (anything is better than nothing)

Work on increasing income: Sometimes the problem isn’t your budget—it’s your income. Can you pick up side work? Ask for a raise? Find a higher-paying job?

The goal isn’t to perfectly hit 50/30/20 right now. The goal is to move toward financial stability at whatever pace you can manage.

Your Next Steps: Start This Week

The 50/30/20 rule won’t fix your finances overnight. But it will give you a framework that’s simple enough to actually follow.

This week:

- Calculate your after-tax monthly income

- Track every expense for 7 days to see where you’re starting

- Calculate your three target numbers (50% needs, 30% wants, 20% savings)

This month:

- Categorize all your expenses honestly

- Compare your current reality to the 50/30/20 targets

- Make one adjustment to get closer to the targets

This quarter:

- Set up automatic transfers for your 20% savings

- Reduce your biggest wants expense by 25%

- Adjust the percentages if needed for your situation (like 60/20/20)

This year:

- Consistently hit your savings target

- Build a 3-6 month emergency fund

- Increase your savings percentage if possible

The beauty of 50/30/20 is that it’s flexible. If you’re doing 65/20/15 right now, that’s fine—you’re still being intentional with your money. If you can only save 10% right now, that’s better than 0%.

The rule is a tool, not a prison. Use it in whatever way actually helps you save more, stress less, and build the financial life you want.

Sources

[1] Warren, Elizabeth and Amelia Warren Tyagi, “All Your Worth: The Ultimate Lifetime Money Plan,” Free Press, 2005

[2] Fidelity Investments, “How much should I save for retirement?” 2025, https://www.fidelity.com/viewpoints/retirement/how-much-do-i-need-to-retire

[3] YNAB (You Need A Budget), Pricing information, accessed February 2026, https://www.ynab.com/pricing

[4] U.S. Bureau of Labor Statistics, “Consumer Expenditure Survey,” 2025, https://www.bls.gov/cex/

[5] U.S. Census Bureau, “Median Household Income,” 2025

[6] Apartment List, “National Rent Report,” January 2026

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Your financial situation is unique, and you should consider consulting with a qualified financial advisor for personalized guidance.

About the Author: The FinanceWise team is dedicated to making personal finance accessible and actionable for young adults. We believe budgeting shouldn’t be restrictive—it should be empowering.