You’re 25, you just got your first “real” job with benefits, and someone told you that you should open an IRA. Great advice. Then they hit you with: “But should you do a Roth or Traditional?”

You stare blankly. What’s the difference? Does it even matter? Can’t you just pick one and deal with it later?

Here’s the truth: this decision will impact how much money you have in retirement by potentially hundreds of thousands of dollars. Choose wrong in your twenties, and you’ll kick yourself in your sixties.

But here’s the good news: for most people in their 20s, the answer is actually pretty clear. And once you understand the fundamental difference between these two accounts, the decision becomes obvious.

I’ve been writing about retirement accounts for years, and I’ve seen too many young people either paralyzed by this choice or randomly picking one without understanding what they’re doing. This guide will break down exactly how Roth and Traditional IRAs work, show you real math on which saves you more money, and help you make the right choice based on your specific situation.

The One Thing You Need to Understand First

Before we dive into Roth vs Traditional, let’s get crystal clear on what an IRA actually is.

IRA = Individual Retirement Account

It’s a special investment account with tax advantages designed to help you save for retirement. You put money in, invest it (usually in stocks, bonds, or index funds), and let it grow for decades until you retire.

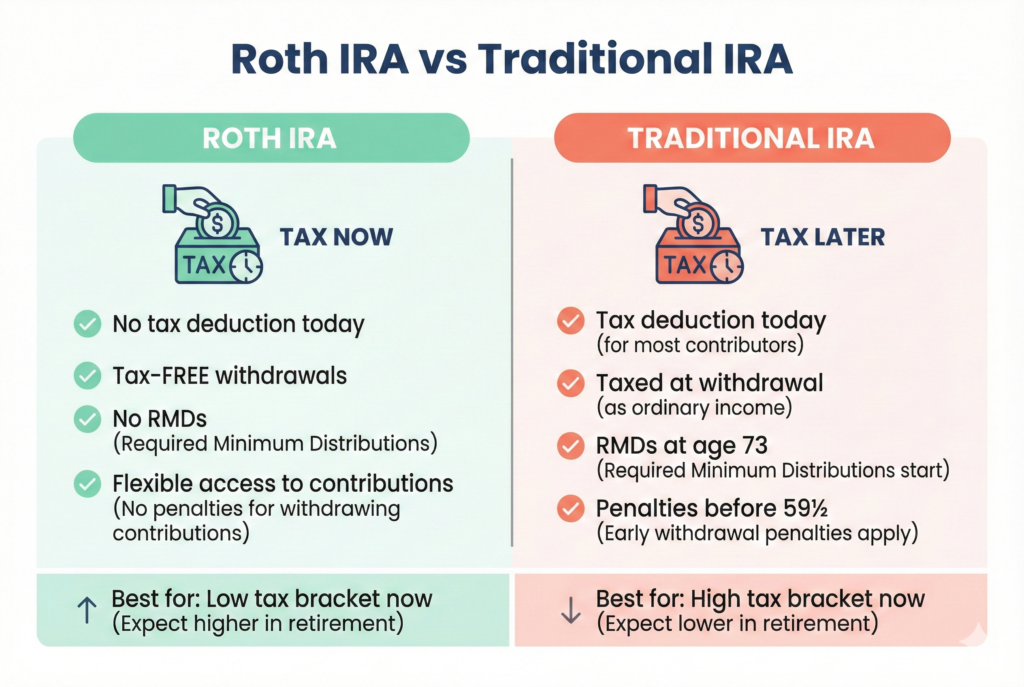

The “Roth vs Traditional” question is really asking: When do you want to pay taxes on this money?

- Traditional IRA: Pay taxes later (when you withdraw in retirement)

- Roth IRA: Pay taxes now (when you contribute)

That’s it. That’s the entire difference. Everything else flows from this one choice.

Let me show you why this matters with a simple example:

Traditional IRA: You contribute $6,000. You get to deduct that $6,000 from your taxes this year (saving you ~$1,320 if you’re in the 22% bracket). That $6,000 grows to $50,000 over 30 years. When you withdraw it, you pay taxes on all $50,000.

Roth IRA: You contribute $6,000 with money you’ve already paid taxes on (no deduction this year). That $6,000 grows to $50,000 over 30 years. When you withdraw it, you pay zero taxes on the $50,000.

See the trade-off? Tax break now vs tax-free growth forever.

How Traditional IRAs Work

A Traditional IRA is the “pay taxes later” option.

The Mechanics

1. You contribute pre-tax dollars (sort of)

Technically, you contribute with after-tax money from your paycheck, but then you deduct the contribution on your tax return. So if you contribute $6,000, your taxable income drops by $6,000.

Example: You earn $60,000. You contribute $6,000 to a Traditional IRA. Your taxable income is now $54,000. At the 22% tax bracket, that saves you $1,320 in taxes this year.

2. Your money grows tax-deferred

Any gains, dividends, or interest you earn inside the account aren’t taxed. You don’t pay capital gains taxes when you sell investments. Everything just compounds.

3. You pay taxes when you withdraw (in retirement)

When you’re 60 or 70 and start withdrawing money, every dollar you pull out counts as ordinary income and gets taxed at whatever your tax rate is then.

Traditional IRA Rules for 2026[1]

Contribution limit: $7,000 per year (or $8,000 if you’re 50+)

Income limits for tax deduction:

- If you’re covered by a workplace retirement plan (401k), the deduction phases out:

- Single: $77,000 – $87,000

- Married filing jointly: $123,000 – $143,000

- If you’re NOT covered by a workplace plan: no income limit (everyone gets the deduction)

Withdrawal rules:

- Penalty-free withdrawals start at age 59½

- You MUST start taking money out (Required Minimum Distributions) at age 73[2]

- Early withdrawals (before 59½) face a 10% penalty plus income tax (with some exceptions)

Who Benefits Most from Traditional IRAs

People in high tax brackets now who expect to be in lower brackets in retirement

Example: You’re a lawyer earning $180,000 (32% tax bracket). In retirement, you expect to live on $60,000/year (12% bracket). Deducting contributions at 32% now and paying 12% later is a huge win.

People who need the tax break today

If you’re struggling financially and that $1,000+ tax refund from the IRA deduction helps you avoid credit card debt, take the Traditional IRA.

People who plan to retire in a state with no income tax

Live in California (13.3% state tax) now but plan to retire in Florida (0% state tax)? That’s a big advantage for Traditional IRAs.

How Roth IRAs Work

A Roth IRA is the “pay taxes now, never again” option.

The Mechanics

1. You contribute after-tax dollars

The money going into your Roth IRA has already been taxed. You don’t get a deduction this year.

Example: You earn $60,000 and contribute $6,000 to a Roth IRA. Your taxable income stays $60,000. You get no tax break.

2. Your money grows completely tax-free

Just like a Traditional IRA, you don’t pay taxes on gains, dividends, or interest while the money grows.

3. You withdraw it all tax-free in retirement

This is the magic. When you’re 65 and your Roth IRA has $500,000 in it, you can withdraw all $500,000 and pay zero taxes. Not a single dollar.

Roth IRA Rules for 2026[1]

Contribution limit: $7,000 per year (or $8,000 if you’re 50+)

Income limits (this is where Roth gets tricky):

- Single filers:

- Full contribution: Under $146,000

- Partial contribution: $146,000 – $161,000

- No contribution allowed: Over $161,000

- Married filing jointly:

- Full contribution: Under $230,000

- Partial contribution: $230,000 – $240,000

- No contribution allowed: Over $240,000

Withdrawal rules:

- You can withdraw your contributions anytime, tax and penalty-free (because you already paid taxes on them)

- Earnings can be withdrawn tax-free after age 59½ AND the account has been open for 5+ years

- NO Required Minimum Distributions—ever. You can leave it growing forever.

Who Benefits Most from Roth IRAs

People in their 20s and early 30s

When you’re young, you’re likely in a lower tax bracket than you’ll be in retirement. Paying taxes at 12% or 22% now beats paying at 24% or 32% later.

People who expect income to increase significantly

If you’re earning $50,000 now but expect to earn $150,000+ later in your career, lock in today’s low tax rate with a Roth.

People who want tax diversification in retirement

Having both pre-tax money (401k, Traditional IRA) and tax-free money (Roth IRA) gives you flexibility. You can manage your tax bracket in retirement by controlling how much you withdraw from each.

People who want to leave money to heirs

Roth IRAs have no Required Minimum Distributions. You can let it grow your entire life and pass it to your kids tax-free.

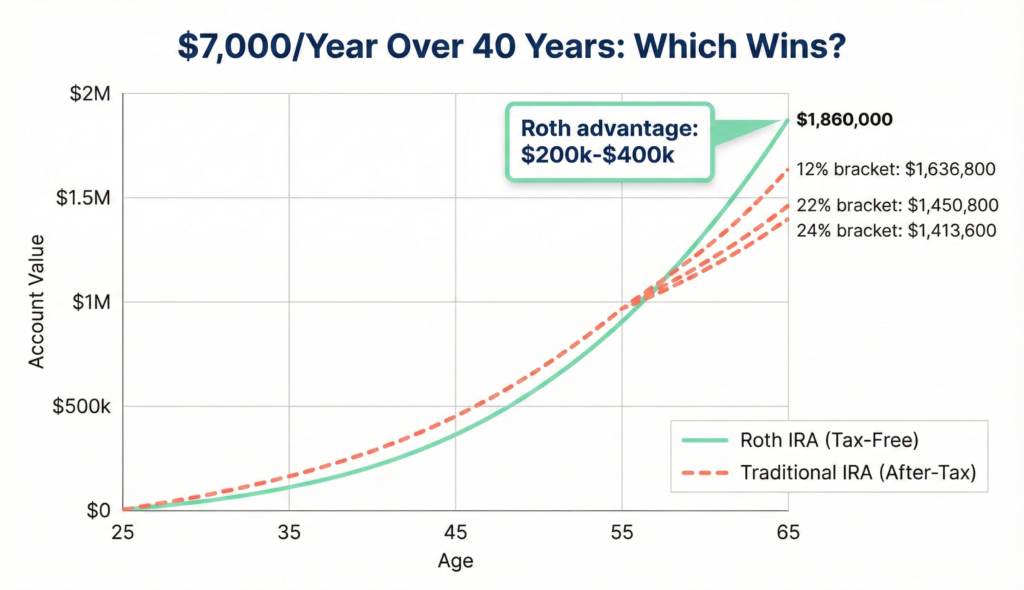

The Math: Which Actually Saves You More Money?

Let’s run real numbers. Assume:

- You’re 25 years old

- You contribute $7,000/year

- Your investments grow 8% annually

- You’re currently in the 22% tax bracket

- You retire at 65 (40 years of contributions)

Scenario 1: Traditional IRA

Contributions: $7,000/year × 40 years = $280,000

Tax savings now: $280,000 × 22% = $61,600 saved over 40 years

Account value at 65: ~$1,860,000 (this is simplified—actual growth varies)

Taxes owed when withdrawing: Depends on your retirement tax bracket

If you’re in the 12% bracket in retirement:

- Taxes owed: $1,860,000 × 12% = $223,200

- Net after taxes: $1,636,800

If you’re in the 22% bracket in retirement (same as now):

- Taxes owed: $1,860,000 × 22% = $409,200

- Net after taxes: $1,450,800

If you’re in the 24% bracket in retirement:

- Taxes owed: $1,860,000 × 24% = $446,400

- Net after taxes: $1,413,600

Scenario 2: Roth IRA

Contributions: $7,000/year × 40 years = $280,000

Tax savings now: $0 (you paid taxes on the contributions)

Account value at 65: ~$1,860,000

Taxes owed when withdrawing: $0

Net after taxes: $1,860,000

The Verdict

Roth wins if:

- Your tax rate in retirement is the same or higher than now

- You value flexibility and no RMDs

Traditional wins if:

- Your tax rate in retirement is significantly lower than now

- You need the tax deduction today

For most people in their 20s: Roth is the better bet. You’re likely in a low tax bracket now, and your income (and tax bracket) will probably increase over your career.

Special Situations and Exceptions

What If You’re a High Earner?

If you earn over $161,000 (single) or $240,000 (married), you can’t contribute directly to a Roth IRA.[1]

Solution: The Backdoor Roth IRA

This is a legal loophole:

- Contribute to a Traditional IRA (this has no income limits if you’re not deducting it)

- Immediately convert it to a Roth IRA

- Pay taxes on the conversion (which is minimal if you convert right away)

It’s perfectly legal and IRS-approved.[3] Millions of high earners do this every year.

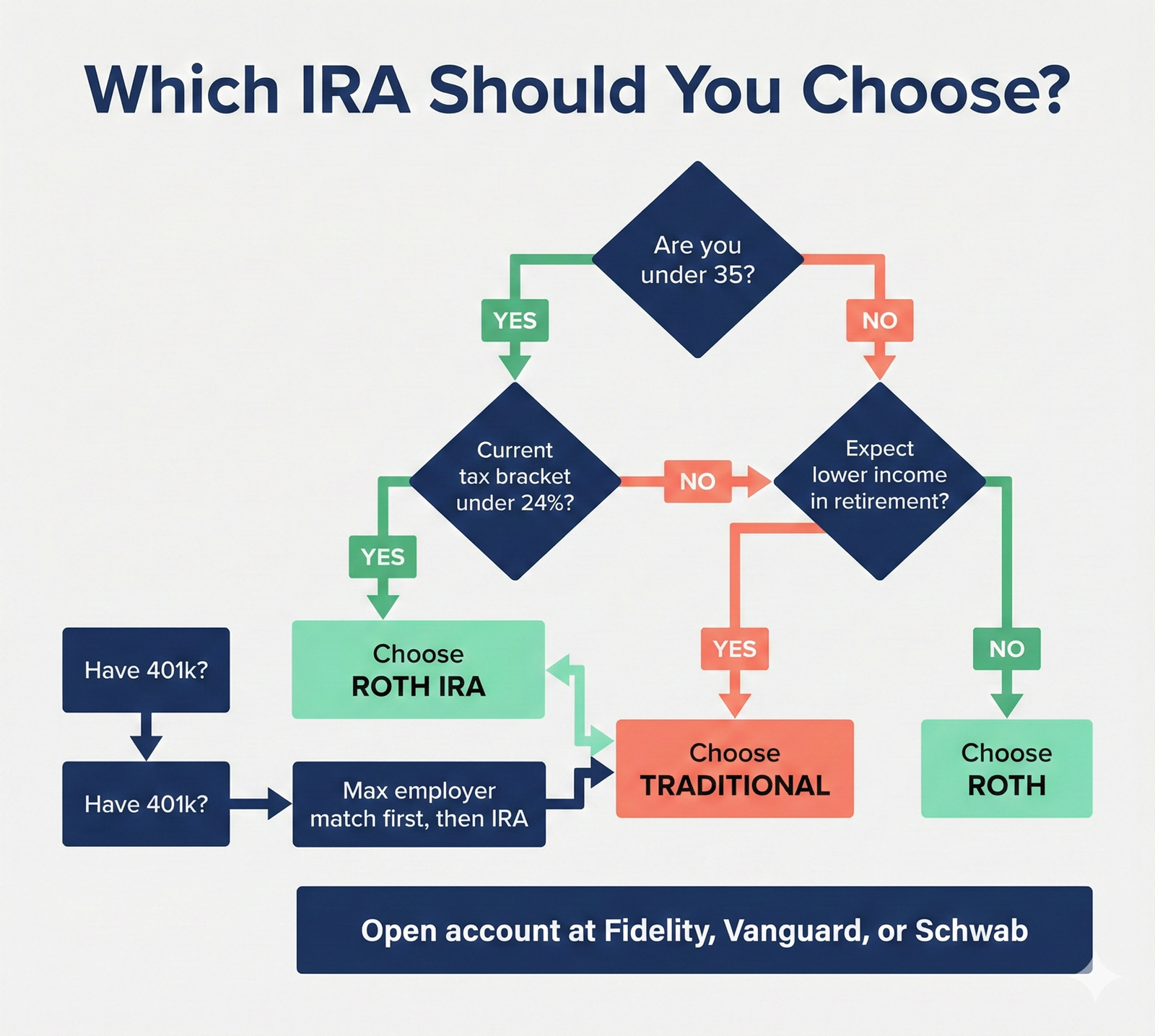

What If You Have a 401(k) at Work?

Great question. Here’s the priority:

Priority 1: Contribute to your 401(k) up to the employer match (that’s free money)

Priority 2: Max out your Roth IRA ($7,000)

Priority 3: Go back and max out your 401(k) ($23,500 total limit)[4]

Why this order? Roth IRAs have better investment options and more flexibility than most 401(k)s.

Can You Do Both Roth and Traditional?

Yes! You can contribute to both in the same year. But the $7,000 limit is combined—not $7,000 per account.

Example:

- $4,000 to Roth IRA

- $3,000 to Traditional IRA

- Total: $7,000 ✓

What About Roth 401(k)?

Many employers now offer Roth 401(k) options. These combine the best of both worlds:

- High contribution limits like a 401(k) ($23,500)

- Tax-free withdrawals like a Roth IRA

If your employer offers this, consider splitting your contributions between Traditional 401(k) (for the match) and Roth 401(k).

Common Mistakes People Make

Mistake #1: Not Contributing Because They Can’t Decide

Analysis paralysis is real. People spend months researching Roth vs Traditional and contribute nothing.

The truth: Either choice is better than no choice. Just pick one and start. You can always open the other type next year.

Mistake #2: Choosing Traditional Just for the Tax Refund

“But I want that $1,540 refund!”

If you’re in the 22% bracket now and will be in the 24% bracket in retirement, that refund will cost you tens of thousands later.

Mistake #3: Not Contributing Because “I’ll Do It Next Year”

Retirement accounts have one superpower: time. Every year you wait costs you years of compound growth you can never get back.

Example: Contribute $7,000 at age 25, and it grows to ~$147,000 by age 65 (at 8% growth). Wait until age 35 to contribute that same $7,000, and it only grows to ~$68,000. That 10-year delay cost you $79,000.

Mistake #4: Withdrawing Early

Life happens. You lose your job, medical emergency, whatever. But if you withdraw from a Traditional IRA before 59½, you pay income tax PLUS a 10% penalty.

Roth IRAs are more forgiving—you can withdraw contributions (not earnings) anytime. But you should still avoid it.

Mistake #5: Not Increasing Contributions Over Time

You start with $100/month. Great! But 5 years later, you’re earning 40% more and still contributing $100/month.

Better approach: Increase your IRA contribution by 1% every time you get a raise.

How to Actually Open and Fund Your IRA

Theory is great. Let’s talk execution.

Step 1: Choose a Brokerage (5 minutes)

Best options for beginners:

- Vanguard: Low fees, great index funds

- Fidelity: No minimums, excellent customer service, great mobile app

- Charles Schwab: No fees, wide investment selection

All three are excellent. Pick one and move on.

Step 2: Open the Account (10 minutes)

Go to the website, click “Open an IRA,” choose Roth or Traditional, and fill out the application. You’ll need:

- Social Security number

- Bank account info for linking

- Employment information

- Beneficiary designation

Step 3: Fund the Account (Instant to 3 days)

Transfer money from your checking account. Most platforms offer:

- One-time transfer

- Automatic monthly contributions (highly recommended)

Pro tip: Set up automatic monthly transfers of $583/month to max out the $7,000 annual limit. Automate it and forget it.

Step 4: Invest the Money (5 minutes)

CRITICAL: Just depositing money into an IRA doesn’t invest it. You have to buy investments.

Simple approach for beginners:

- Buy a Target-Date Fund (like “Vanguard Target Retirement 2065”)

- It automatically invests in a diversified mix of stocks and bonds

- It adjusts to become more conservative as you age

Or buy an S&P 500 Index Fund:

- Vanguard: VFIAX or VOO

- Fidelity: FXAIX

- Schwab: SWPPX

Either approach works. The important thing is actually investing the money, not letting it sit as cash.

Step 5: Increase Contributions When You Can

Got a raise? Increase your monthly IRA contribution immediately. Received a bonus? Dump it into your IRA.

The $7,000 limit isn’t a target—it’s a ceiling. If you can max it out, do it. If not, contribute what you can and increase over time.

Real Talk: Why Most People in Their 20s Should Choose Roth

After analyzing thousands of financial situations, here’s my honest recommendation:

If you’re under 35 and earning less than $100,000, choose a Roth IRA.

Why?

1. You’re probably in a lower tax bracket now than you’ll ever be again

Entry-level salary at 22% bracket? In 20 years, you’ll likely be in 24% or 32% bracket. Lock in today’s low rate.

2. Tax-free growth for 40+ years is insanely powerful

A 25-year-old contributing $7,000/year until 65 ends up with ~$1.86 million tax-free. That’s life-changing money.

3. Flexibility matters

Roth contributions can be withdrawn anytime. Traditional IRA has penalties. If you’re young and life is unpredictable, that flexibility is valuable.

4. No Required Minimum Distributions

Roth IRAs don’t force you to take money out. You can let it grow forever or pass it to your kids.

5. Tax diversification

If you have a Traditional 401(k) at work, having a Roth IRA gives you tax diversity in retirement—options are valuable.

Your Action Plan: Open Your IRA This Week

Stop researching. Stop overthinking. Here’s what you do:

Today:

- Decide: Roth or Traditional (if you’re under 35, probably Roth)

- Choose a brokerage: Fidelity, Vanguard, or Schwab

- Go to their website and click “Open an IRA”

This week:

- Complete the application (10 minutes)

- Link your bank account

- Make your first contribution (even if it’s just $50)

This month:

- Set up automatic monthly contributions

- Invest the money (don’t leave it as cash)

- Add it to your 50/30/20 budget as part of your 20% savings

This year:

- Try to contribute at least $3,500 (50% of the limit)

- Increase contributions when you get a raise

- Check your account quarterly—not daily

The difference between someone who opens an IRA at 25 vs 35 is over $500,000 by retirement. That’s not a typo. Ten years of compound growth is worth half a million dollars.

You don’t need to be rich to start. You don’t need to max it out immediately. You just need to start.

Open the account. Make the first contribution. Let time and compound interest do the rest.

Sources

[1] Internal Revenue Service, “401(k) limit increases to $23,500 for 2026, IRA limit rises to $7,000,” November 2025, https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2026

[2] Internal Revenue Service, “Retirement Plan and IRA Required Minimum Distributions FAQs,” accessed February 2026, https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

[3] Internal Revenue Service, “Roth IRAs,” Publication 590-A, 2025, https://www.irs.gov/publications/p590a

[4] Internal Revenue Service, “Retirement Topics – 401(k) and Profit-Sharing Plan Contribution Limits,” accessed February 2026, https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-401k-and-profit-sharing-plan-contribution-limits

[5] Vanguard, “Roth vs. Traditional IRA: Which is right for you?” Investor Education, 2025

[6] Fidelity Investments, “IRA Contribution Limits and Deadlines,” 2026, https://www.fidelity.com/retirement-ira/contribution-limits-deadlines

[7] U.S. Government Accountability Office, “Retirement Security: Trends in Retirement Account Balances,” December 2025

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or investment advice. Retirement account rules are complex and change frequently. Consider consulting with a qualified financial advisor or tax professional for personalized guidance based on your specific situation.

About the Author: The FinanceWise team is dedicated to making retirement planning accessible and actionable for young adults. We believe starting early with the right account can mean the difference between a comfortable retirement and struggling in your 60s.