You’re 24, renting your first apartment without roommates, and you just spent $3,000 furnishing it. Your laptop cost $1,200. Your TV was $800. Your phone, bike, clothes, furniture—if you added it all up, you probably have $15,000-25,000 worth of stuff.

Then one night, you come home and your apartment door is wide open. Someone broke in and took everything valuable. You call your landlord, devastated, asking if their insurance will cover your stolen belongings.

They say: “My insurance only covers the building. Your stuff? That’s on you.”

This actually happens. All the time. And most renters have no idea their landlord’s insurance doesn’t protect their personal belongings—until it’s too late.

Here’s the truth: renters insurance costs about as much as two coffees per month, yet 55% of renters don’t have it.[1] They think they don’t need it, can’t afford it, or assume their landlord’s policy covers them. All three assumptions are wrong.

This guide will show you exactly what renters insurance covers, what it costs, how to get it, and why skipping it is one of the riskiest financial decisions you can make as a renter.

What Is Renters Insurance?

Renters insurance is a policy that protects your personal belongings and provides liability coverage when you rent an apartment, house, or condo.

Think of it as three types of protection bundled into one affordable policy:

1. Your stuff (personal property coverage) 2. Your liability (if someone gets hurt in your apartment) 3. Your temporary housing (if your place becomes unlivable)

Your landlord’s insurance covers the building structure—walls, roof, floors, appliances they own. But everything you own inside? That’s your responsibility.

Maria, a 27-year-old teacher in Denver, learned this the hard way. A pipe burst in the apartment above hers, flooding her unit and destroying her furniture, laptop, and clothes. “I thought my landlord’s insurance would cover it,” she said. “Nope. They fixed the building damage, but I lost $8,000 worth of belongings and got nothing back. I didn’t have renters insurance because I thought I was ‘saving money.’ That decision cost me an entire year’s salary in losses.”

Discover What Renters Insurance Actually Covers

Let’s break down the three main components:

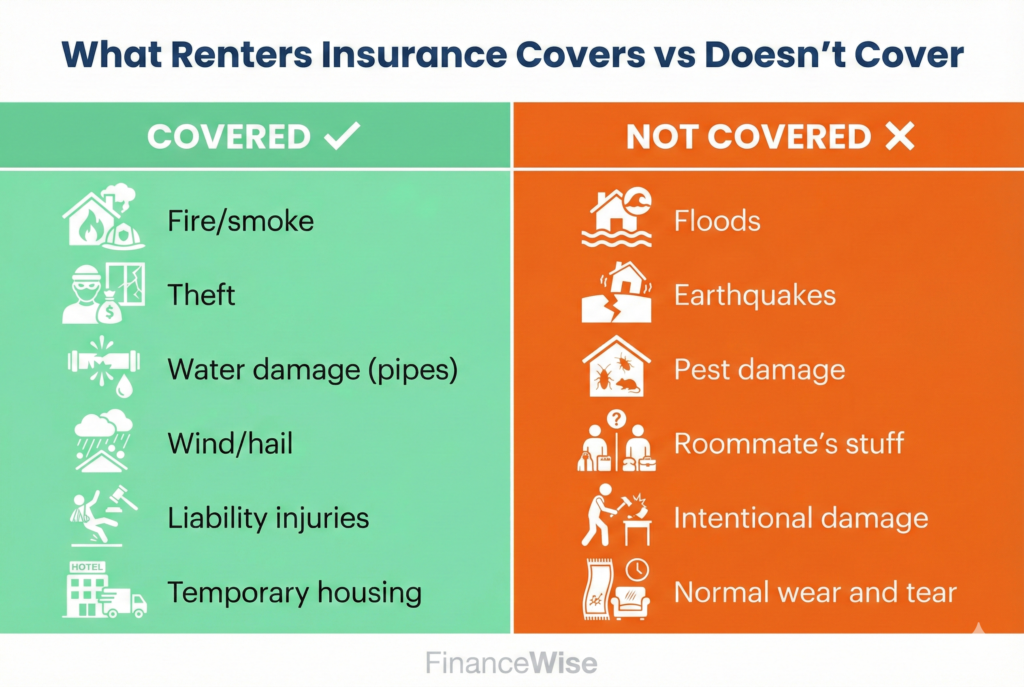

1. Personal Property Coverage

This covers your belongings if they’re damaged or stolen due to covered perils.

What’s covered:[2]

- Furniture: Couch, bed, desk, chairs, tables

- Electronics: Laptop, TV, gaming console, phone, tablet

- Clothing and shoes: Your entire wardrobe

- Jewelry and watches: Up to a certain limit (usually $1,500)

- Kitchen items: Dishes, small appliances, cookware

- Sports equipment: Bike, ski gear, camping equipment

- Textbooks and school supplies

- Décor: Art, rugs, lamps, mirrors

Covered perils include:

- Fire or smoke damage

- Theft or vandalism

- Water damage from burst pipes (not floods)

- Wind or hail damage

- Damage from riots or civil unrest

- Falling objects

- Electrical surges

What’s NOT covered:

- Flood damage (you need separate flood insurance)

- Earthquake damage (separate policy needed)

- Damage from pests or bedbugs

- Normal wear and tear

- Intentional damage you caused

Off-premises coverage: Your stuff is even covered outside your apartment. If your laptop gets stolen from your car or someone breaks into your gym locker, you’re covered up to your policy limits.

2. Liability Coverage

This protects you if someone gets injured in your apartment or if you accidentally damage someone else’s property.

Real scenarios where this matters:

Scenario 1: Your friend trips over your rug, breaks their wrist, and their medical bills hit $15,000. Without renters insurance, they could sue you. With liability coverage (typically $100,000-$300,000), your insurance pays.

Scenario 2: Your bathtub overflows while you’re gone, flooding the apartment below you and destroying your downstairs neighbor’s furniture. Your liability coverage pays for their damages.

Scenario 3: Your dog bites a visitor. Their medical bills and potential lawsuit? Covered by your renters insurance.

Liability coverage also includes legal defense costs if someone sues you. Even if the lawsuit is bogus, legal fees can hit $10,000+. Your insurance handles that.

3. Additional Living Expenses (ALE)

If your apartment becomes unlivable due to a covered event (fire, major water damage, etc.), this pays for your temporary housing and related costs.

What’s covered:

- Hotel or temporary rental costs

- Restaurant meals (if you can’t cook)

- Pet boarding

- Laundry costs

- Storage fees for your belongings

Example: A fire makes your apartment uninhabitable for two months. Your renters insurance pays for a hotel, meals out, and storage—potentially $3,000-5,000 in expenses you’d otherwise pay out of pocket.

Limit: Usually 20-30% of your personal property coverage. If you have $30,000 in coverage, you get $6,000-9,000 for temporary living expenses.

How Much Does Renters Insurance Actually Cost?

Here’s the good news: it’s shockingly affordable.

National average: $15-30 per month ($180-360 per year)[3]

Cost by state (2026):[3]

- Cheapest states: North Dakota ($12/month), South Dakota ($13/month), Wyoming ($14/month)

- Most expensive states: Louisiana ($28/month), Oklahoma ($27/month), Mississippi ($26/month)

- Major cities: New York ($18-25/month), Los Angeles ($16-22/month), Chicago ($14-20/month)

What affects your price:

- Location: High-crime areas cost more

- Coverage amount: $30,000 coverage vs $50,000 coverage

- Deductible: $500 deductible vs $1,000 deductible

- Credit score: Better credit = lower rates

- Safety features: Smoke alarms, security system, deadbolts can get you discounts

- Bundling: Get it from the same company as your car insurance for a discount (often 10-25%)

Example breakdown:

- $30,000 personal property coverage

- $100,000 liability coverage

- $500 deductible

- Chicago apartment

- Cost: ~$17/month

That’s $204 per year to protect $30,000+ worth of belongings. That’s 0.68% of your coverage amount. Compare that to car insurance (often 5-10% of your car’s value) or health insurance.

Do You Actually Need Renters Insurance?

Short answer: If you can’t afford to replace everything you own tomorrow, yes.

Let’s do a reality check. Walk through your apartment right now and add up the replacement cost of:

- Your furniture

- All your electronics

- Your entire wardrobe

- Kitchen items

- Bike or sports equipment

- Books and personal items

Most people are shocked. “I thought I only had like $5,000 worth of stuff.” Then they actually inventory it and realize they have $20,000-30,000.

When You Absolutely Need It

You’re required to have it Many landlords now require renters insurance as part of the lease. If you don’t get it, you can’t move in or could face eviction.

You have roommates If your roommate’s candle starts a fire that destroys the apartment, you need liability coverage. Also, their guests could sue you if injured.

You live in a high-crime area Theft is one of the most common renters insurance claims. In 2025, there were over 1.4 million burglaries in the US.[4]

You can’t afford to replace everything If losing all your belongings would financially devastate you, you need insurance.

You have valuable items Laptop, bike, camera equipment, jewelry—these add up fast.

When You Might Skip It (But Probably Shouldn’t)

You literally own almost nothing Like, you have a mattress on the floor, a used laptop, and some clothes from Goodwill. Even then, replacing it all would still cost $2,000-3,000.

You’re moving in a week If you’re between apartments for a very short period, maybe. But get coverage immediately when you move in.

Even if you decide you don’t need property coverage, you still need liability coverage. One lawsuit from a guest getting injured could bankrupt you.

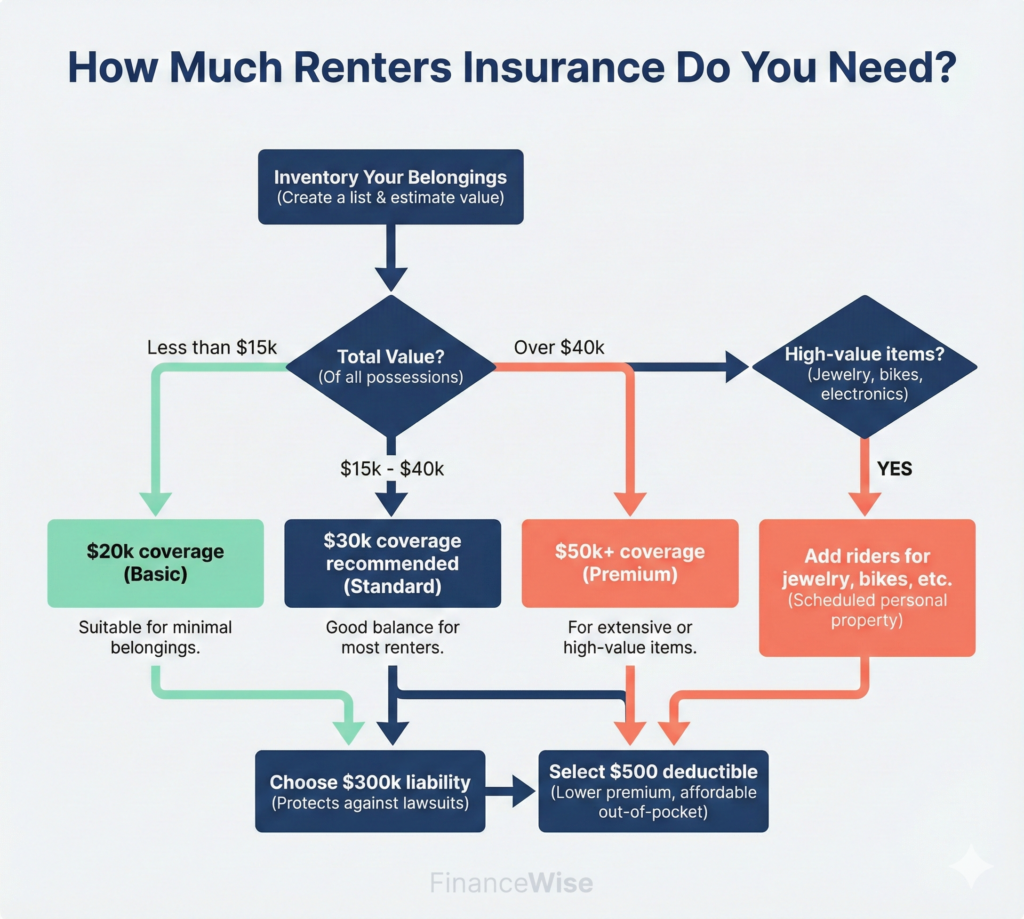

How Much Coverage Do You Need?

Don’t just guess. Here’s how to calculate it properly.

Step 1: Inventory Your Belongings

Go room by room and list everything valuable:

Bedroom:

- Bed frame and mattress: $800

- Dresser and nightstand: $400

- Laptop: $1,200

- Phone: $800

- Clothes and shoes: $3,000

- Subtotal: $6,200

Living room:

- Couch: $1,200

- TV: $600

- Coffee table and décor: $300

- Gaming console: $500

- Subtotal: $2,600

Kitchen:

- Dishes, pots, small appliances: $400

Other:

- Bike: $600

- Outdoor/sports equipment: $400

- Misc: $800

Total: ~$11,000

Most renters discover they have $15,000-30,000 worth of belongings. Round up and add a buffer for things you forgot.

Step 2: Choose Replacement Cost vs Actual Cash Value

Actual Cash Value (ACV): Pays you what your stuff is worth today (depreciated)

- Your 3-year-old laptop originally cost $1,200 but is worth $400 now. You get $400.

Replacement Cost: Pays to replace your stuff with new items

- Your 3-year-old laptop gets you a new $1,200 laptop.

Price difference: Replacement Cost coverage costs about 10% more but is absolutely worth it. Don’t skimp here.

Step 3: Determine Liability Coverage

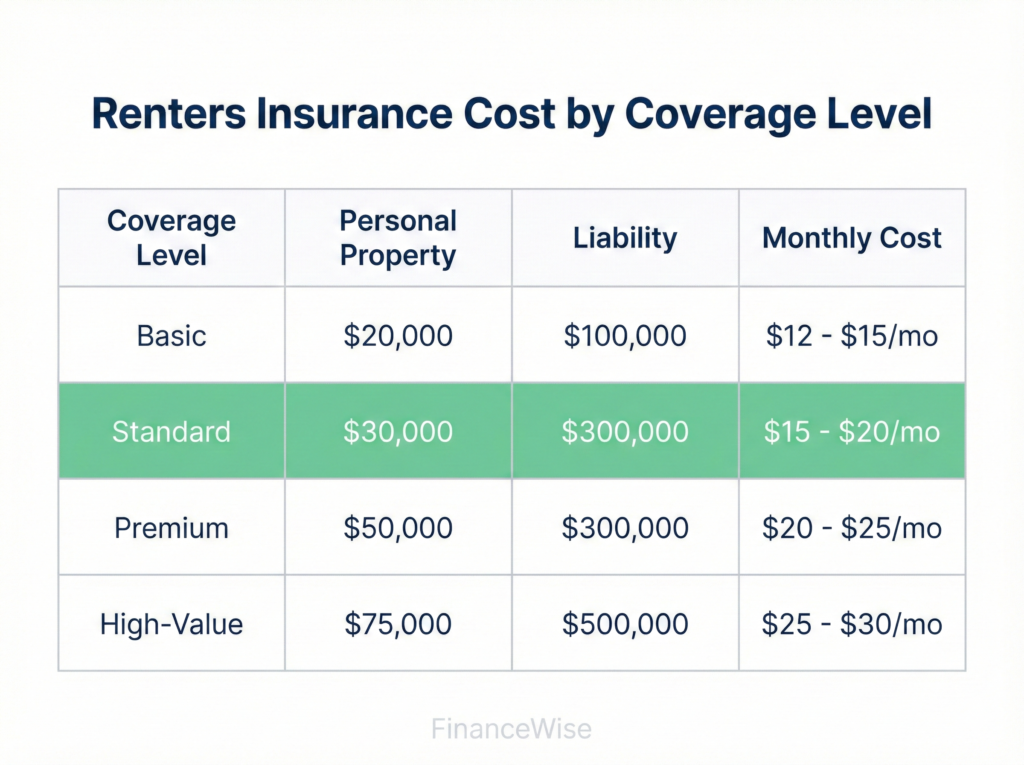

Standard options:[2]

- $100,000 (minimum recommended)

- $300,000 (better)

- $500,000 (if you have significant assets to protect)

My recommendation: Get at least $300,000. The difference in cost between $100k and $300k is often only $2-3/month, and it’s worth the peace of mind.

Step 4: Choose Your Deductible

Common deductibles: $250, $500, $1,000

How it works: You pay this amount before insurance kicks in.

Example: Someone steals your $1,500 bike. With a $500 deductible, you pay $500 and insurance pays $1,000.

Strategy:

- Lower deductible ($250-500) = Higher monthly premium

- Higher deductible ($1,000) = Lower monthly premium

Choose a deductible you could afford to pay if you had to file a claim tomorrow.

Common Renters Insurance Mistakes

Mistake #1: “I Don’t Have Anything Valuable”

Yes, you do. Your laptop, phone, bike, clothes, furniture—it all adds up. Most people have $15,000-30,000 in belongings and just don’t realize it.

Mistake #2: Underinsuring High-Value Items

Standard policies have limits on certain categories:

- Jewelry: Usually $1,500 limit

- Bicycles: Often $1,000-2,000 limit

- Cash: $200 limit

- Collectibles: $2,500 limit

Have a $3,000 engagement ring? Add a “rider” or “endorsement” to specifically cover it. Costs about $1-2 per $100 of value.

Mistake #3: Not Updating Coverage When You Buy Expensive Items

Bought a $2,000 camera? New $4,000 bike? Update your policy. Don’t wait until it’s stolen to realize you’re underinsured.

Mistake #4: Filing Small Claims

Don’t file a claim for a $300 loss if your deductible is $500. You pay the whole thing anyway, and filing a claim can increase your rates.

When to file: Only when the loss exceeds your deductible by a meaningful amount ($1,000+).

Mistake #5: Assuming Your Roommate’s Policy Covers You

Nope. Each person needs their own policy. If there are three roommates, you need three separate renters insurance policies.

How to Get Renters Insurance (Step-by-Step)

Here’s the actual process:

Step 1: Get Quotes (15 minutes)

Best companies for renters:[5]

- State Farm: Great coverage, local agents, bundling discounts

- Lemonade: Fully digital, fast claims, affordable, great for tech-savvy renters

- Allstate: Strong customer service, good bundling discounts

- USAA: Best rates (if you’re military or family of military)

- Nationwide: Good coverage options, solid reputation

How to compare:

- Go to 3-4 company websites

- Enter your info (address, coverage amount, deductible)

- Get instant quotes

- Compare apples to apples (same coverage amounts)

Don’t just pick the cheapest. Check reviews, claims process reputation, and customer service quality.

Step 2: Decide on Coverage (5 minutes)

Based on your inventory:

- Personal property: $20,000-50,000 (most common: $30,000)

- Liability: $300,000 recommended

- Type: Replacement cost (not actual cash value)

- Deductible: $500 (good balance)

Step 3: Buy the Policy (10 minutes)

Most companies let you buy online instantly. You’ll need:

- Your address

- Move-in date

- Desired coverage amounts

- Payment info (credit card or bank account)

You can often start coverage the same day or choose a future date.

Step 4: Add It to Your Monthly Budget

50/30/20 budget: This goes in your 50% “Needs” category, not Wants. It’s essential protection, like health insurance.

Example budget impact:

- Rent: $1,400

- Utilities: $120

- Groceries: $300

- Renters insurance: $18

- Total needs: Still well within budget

Step 5: Document Your Belongings

Take photos or videos of your apartment and all valuable items. Store them in the cloud (Google Drive, Dropbox). If you ever need to file a claim, this makes it much easier to prove what you owned.

Pro tip: Keep receipts for expensive items (electronics, furniture, jewelry).

Special Situations

What If Your Landlord Requires It?

Many landlords now mandate renters insurance. It’s in your lease. If you don’t get it, you could:

- Be denied the apartment

- Face eviction

- Owe damages from the lease

Just get it. It protects you anyway.

What If You Have a Dog?

Some breeds (pit bulls, Rottweilers, German shepherds) are considered “high-risk” and some insurers won’t cover you or charge more.

Solutions:

- Look for pet-friendly insurers

- Get liability coverage through a specialty provider

- Provide proof of training or temperament testing

What If You’re Subletting or Staying Short-Term?

You still need coverage. Many companies offer month-to-month policies with no long-term commitment.

What If You Move?

Call your insurance company and update your address. Your rate might change based on your new location, but you keep the same policy.

What About Bundling with Car Insurance?

If you have car insurance, get your renters insurance from the same company. You’ll usually save 10-25% on both policies.

Example:

- Car insurance alone: $120/month

- Renters insurance alone: $20/month

- Bundled: Car $105/month + Renters $15/month = $120/month total (save $20/month)

That’s $240/year in savings just for bundling.

Your Next Steps: Get Covered This Week

Renters insurance is one of those things people put off until it’s too late. Don’t be that person who learns about coverage the hard way.

Today:

- Inventory your belongings (take 20 minutes, walk through your apartment)

- Calculate what it would cost to replace everything

- Realize you probably have $15,000-30,000 worth of stuff

This week:

- Get quotes from State Farm, Lemonade, and Allstate

- Choose $30,000 personal property, $300,000 liability, $500 deductible

- Buy the policy online (takes 10 minutes)

- Add $15-25/month to your budget

This month:

- Take photos/videos of your apartment and belongings

- Save receipts for any new purchases

- Add coverage to your lease documentation

Ongoing:

- Update your policy when you buy expensive items

- Review coverage annually

- Bundle with car insurance to save money

The $18/month you spend on renters insurance could save you $20,000+ if something goes wrong. That’s a 1,100x return on investment if you ever need to file a claim.

You insure your car. You insure your health. Why wouldn’t you insure everything you own in your apartment?

Get covered. It’s cheaper than you think and more important than you realize.

Sources

[1] Insurance Information Institute, “Facts + Statistics: Renters and Homeowners Insurance,” 2025, https://www.iii.org/fact-statistic/facts-statistics-renters-and-homeowners-insurance

[2] National Association of Insurance Commissioners (NAIC), “Renters Insurance Consumer Guide,” 2025, https://content.naic.org/consumer/renters-insurance.htm

[3] Insurance Information Institute, “Average Cost of Renters Insurance by State,” 2026 data

[4] Federal Bureau of Investigation, “Crime in the United States 2025: Burglary Statistics,” https://ucr.fbi.gov/crime-in-the-u.s/2025/crime-in-the-u.s.-2025/topic-pages/burglary

[5] J.D. Power, “2025 U.S. Homeowners Insurance Study,” J.D. Power and Associates, 2025

[6] State Farm, “Renters Insurance Coverage and Cost Information,” accessed February 2026, https://www.statefarm.com/insurance/home-and-property/renters

[7] Lemonade Insurance, “How Much Does Renters Insurance Cost?” 2026, https://www.lemonade.com/renters-insurance/cost/

Disclaimer: This article is for educational purposes only and does not constitute insurance or legal advice. Renters insurance policies vary by provider and state. Always read your policy documents carefully and consult with a licensed insurance agent for personalized guidance.

About the Author: The FinanceWise team is dedicated to making insurance accessible and understandable for young renters. We believe everyone deserves affordable protection for their belongings and financial security.