Debt Trap Escape: Crush Your 2026 Credit Card Balances

With average credit card interest rates hovering near 25%, carrying a balance is no longer just an inconvenience—it is a financial emergency. Discover the mathematical strategies everyday Americans are using to break free from the minimum payment cycle and reclaim their paychecks.

FinanceWise Editorial Board

Consumer Debt & Budgeting Strategies

Table of Contents

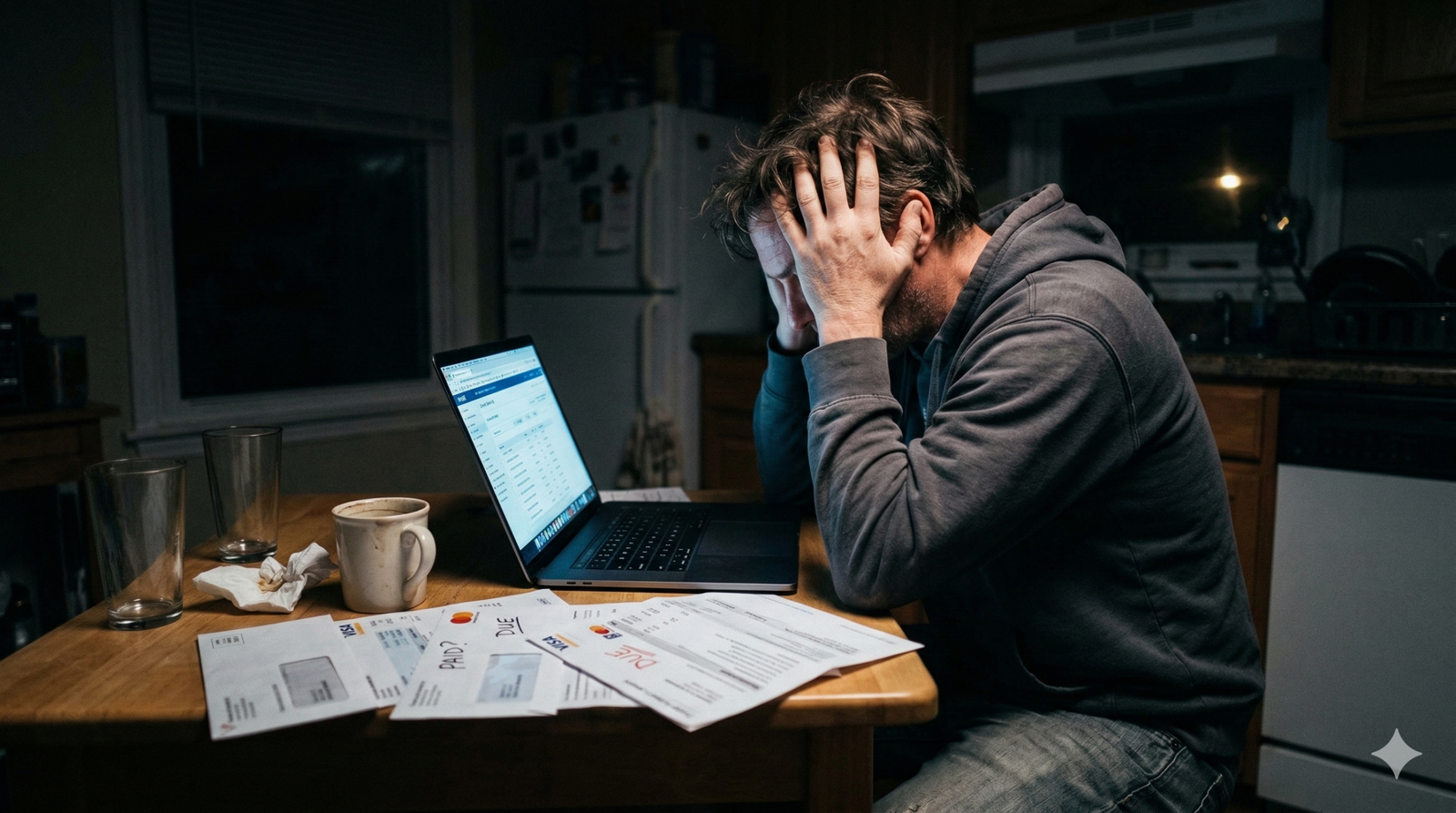

Executing a successful Debt Trap Escape is the single most critical financial move you can make in 2026. If you are earning a median salary—working hard 40 hours a week just to watch a massive chunk of your paycheck vanish into credit card interest—you are not alone. Record-high inflation over the past few years forced millions of middle-class families to put groceries, gas, and medical bills on plastic just to survive.

But here is the harsh mathematical reality: the banks are relying on you to stay comfortable. With national average credit card Annual Percentage Rates (APRs) skyrocketing to nearly 25%, the rules of debt have fundamentally changed. Carrying a $10,000 balance is no longer a minor monthly budget item. It is a compounding financial virus that mathematically guarantees you will never build wealth, buy a home, or retire comfortably until it is eliminated.

With average APRs at record highs, credit card balances act as a regressive tax on the middle class.

The Anatomy of the Minimum Payment Trap

To defeat the enemy, you must understand how their weapon works. Credit card companies are not charities; they are highly sophisticated profit engines. The “Minimum Payment Due” printed on your statement is not a friendly suggestion to help you manage your cash flow. It is a carefully calculated formula designed to keep you in debt for the maximum legal duration.

Typically, a minimum payment is calculated as just 1% to 2% of your total balance, plus the interest charged that month. This means that when you send the bank $150, only $10 or $20 might actually go toward reducing what you owe. The remaining $130 is pure profit for the bank. You are essentially renting your own debt.

Expert Insight: The 15-Year Sentence

“If you have a $8,000 balance at 24% APR and only pay the minimum $160 each month, it will take you over 15 years to pay it off. Worse, you will pay over $11,000 in interest alone. You end up paying $19,000 for $8,000 worth of purchases. This isn’t poor budgeting; this is mathematical servitude.”

The Cost of Paying the Minimum

Scenario: $10,000 Debt at 24% APR. Comparing two payment strategies.

Pure CSS Visualization: Paying an extra $300 a month saves you 20 years of your life and $15,600 in cash.

Real-World Impact: Two Escape Plans

Abstract math is one thing, but how does this work on a real, middle-class salary? The secret to escaping the trap is choosing the psychological or mathematical strategy that fits your personality. Let’s look at two common scenarios.

Case Study: Emma vs. Luis & Maria

Emma, 28

Graphic Designer ($52k/yr)

- Total CC Debt: $8,500

- Card 1 (Store): $500 (29% APR)

- Card 2 (Visa): $8,000 (22% APR)

Emma needs a psychological win. She pauses her investments and throws every spare dollar at the $500 store card while paying minimums on the Visa. She clears the $500 card in 6 weeks. The emotional boost of seeing an account hit “$0” gives her the fierce momentum needed to tackle the $8,000 balance next.

Luis & Maria

Nurse & Admin ($95k Joint)

- Total CC Debt: $22,000

- Card 1 (Medical): $15,000 (25% APR)

- Card 2 (Travel): $7,000 (18% APR)

Luis has a good credit score (720+). They open a new credit card offering a 0% APR Balance Transfer for 18 months. They transfer the toxic $15k balance. They now pay $0 in interest on that money, allowing their $900/month aggressive payment to melt the principal directly. Math beats emotion here.

The Debt Annihilation Matrix

There is no “one size fits all” way to get out of debt. The best method is the one you will actually stick to when you are exhausted on a Friday night and tempted to order $40 takeout on your credit card. Here are the three proven frameworks to execute your escape.

Choose Your Escape Route

The Debt Snowball

List debts from smallest balance to largest, ignoring interest rates. Pay minimums on everything except the smallest. Once paid, roll that money into the next smallest. Builds massive psychological momentum.

The Debt Avalanche

List debts from highest interest rate to lowest. Attack the 29% APR card first, even if it’s your largest balance. It takes longer to see an account close, but saves you the most money in the long run.

0% Balance Transfer

Move high-interest debt to a 0% introductory APR card (usually 12-18 months). Pay a 3% transfer fee upfront, but stop paying 25% monthly interest. Warning: You must pay it off before the 0% period ends!

Actionable Steps to Start Today

Reading about getting out of debt feels good. Actually doing it requires sacrifice. Here is your immediate, 3-step action plan to initiate your debt trap escape today:

- The Plastic Freeze: You cannot dig yourself out of a hole while still holding a shovel. Take your credit cards out of your wallet, delete them from Apple Pay/Google Wallet, and remove them from your Amazon account. Switch 100% to a debit card today.

- The ‘Four Walls’ Budget: Cut every single subscription, streaming service, and restaurant meal. Your income must only cover the ‘Four Walls’ first: Food (groceries only), Shelter, Utilities, and basic Transportation. Every remaining dollar is deployed as a weapon against your debt.

- The Temporary Income Sprint: You cannot always cut your way to wealth; sometimes you have to earn your way out. Whether it is driving for Uber, taking weekend overtime, or selling unused items on Facebook Marketplace, generate an extra $500 this month and throw it directly at the principal.

The road to a zero balance is exhausting. It requires saying “no” to vacations and dinners out while your friends are swiping their cards without a care. But remember: those friends are likely drowning in the exact same 25% APR trap. When you execute this escape plan, the money you free up becomes the foundation for your emergency fund, your investments, and ultimately, your financial peace.

Financial, Credit & YMYL Disclaimer

The content provided on FinanceWise is for informational and educational purposes only and should not be construed as professional financial, legal, or credit counseling advice. Credit card terms, Annual Percentage Rates (APRs), and balance transfer promotions are subject to rapid change and strict terms and conditions. The interactive Debt Freedom Calculator uses simplified mathematical models (ignoring compound frequency variations and promotional periods) and is not a guarantee of payoff timelines. Always consult with a Certified Financial Planner (CFP®) or a certified non-profit credit counselor before making drastic financial decisions, restructuring debt, or taking out new credit lines.

The Debt Freedom Calculator

Stop guessing. Input your real numbers below to see exactly when you will be debt-free and how much interest the bank is currently stealing from you.

Note: This calculator assumes a fixed monthly payment and constant interest rate without any additional charges or late fees. Actual payoff times may vary slightly based on how your specific bank compounds interest (daily vs. monthly).