AI Energy Infrastructure 2026: 3 Proven Ways to Profit

Retail investors are still relentlessly bidding up software and microchip stocks. Meanwhile, institutional capital is quietly front-running the greatest physical bottleneck of the 21st century. If you want to capitalize on artificial intelligence, you must stop looking at the silicon and start looking at the power grid.

Over the past 24 months, the financial media has been overwhelmingly captivated by the generative artificial intelligence boom. Valuations for hyperscale cloud providers and semiconductor designers have shattered historical models. However, a profound shift is currently occurring on the Bloomberg terminals of elite family offices. The institutional narrative has violently pivoted from “Who has the best AI model?” to a much more terrifying question: “Who has the electricity to actually run them?”

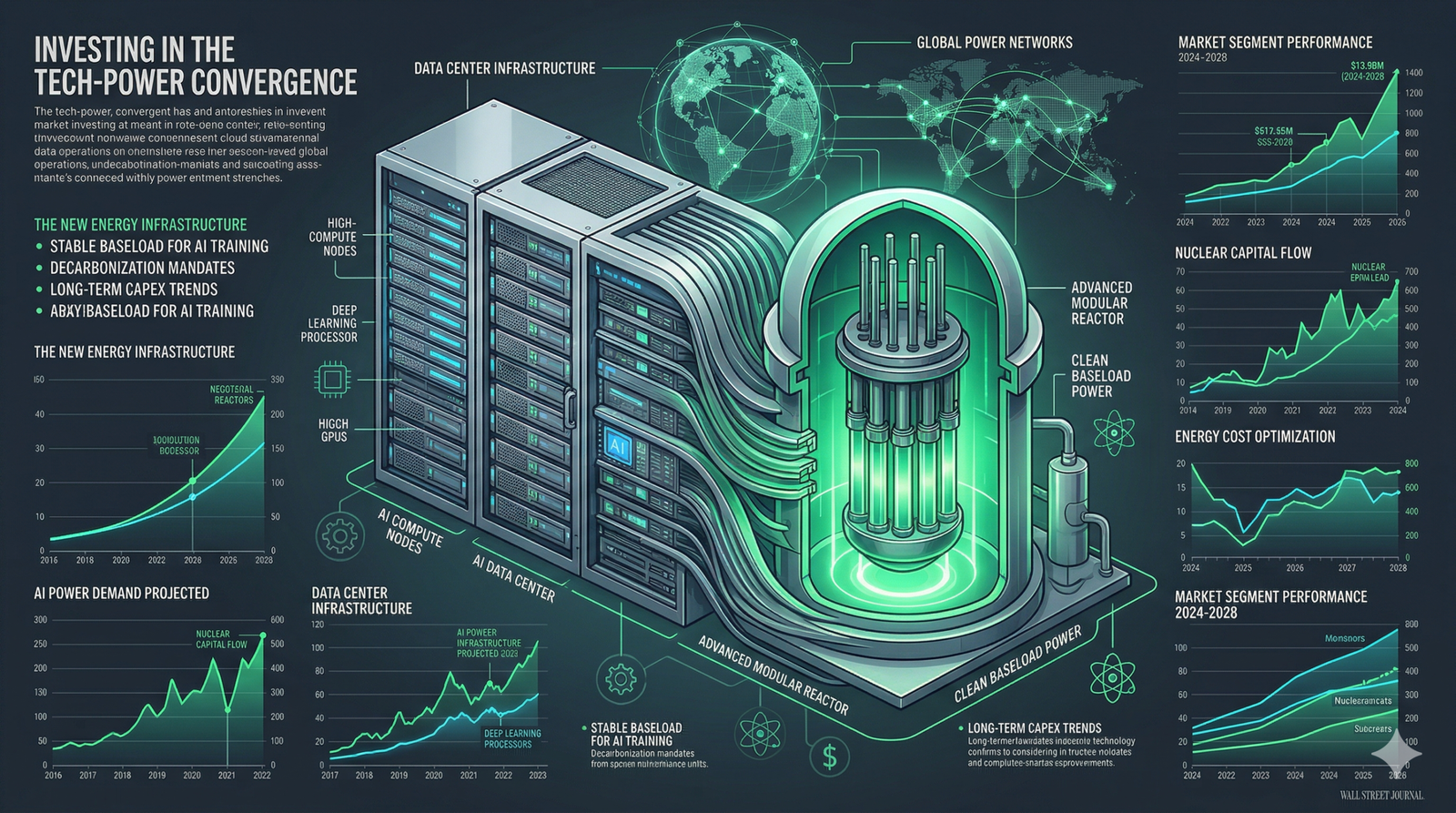

The AI energy infrastructure 2026 crisis is no longer a theoretical projection; it is a mathematical certainty. Artificial intelligence queries require exponentially more power than standard internet searches. As hyperscalers race to build billion-dollar data centers housing hundreds of thousands of GPUs, they are slamming into the physical limitations of an antiquated United States electrical grid that has barely been upgraded since the 1970s.

Table of Contents

- ▪ 1. The Bloomberg Reality Check: The Gigawatt Deficit

- ▪ 2. Proven Strategy 1: The Nuclear Renaissance & SMRs

- ▪ 3. Proven Strategy 2: Grid Modernization & Commodities

- ▪ 4. Proven Strategy 3: Power-Secured Real Estate (REITs)

- ▪ 5. The Institutional Pivot: Moving Beyond Public Tech

- ▪ 6. Interactive: The Infrastructure Alpha Calculator

The Infrastructure Alpha Matrix

1. The Nuclear Fix

Tech giants require 99.999% uptime, impossible with just solar/wind. Capital is violently rotating into physical Uranium (U3O8) trusts and SMR technology.

2. The Copper Squeeze

A $2T grid overhaul is required. Copper, transformers, and switchgears are the ultimate “pick and shovel” plays facing severe structural supply deficits.

3. Power-Secured REITs

Land is cheap; power is priceless. Data center REITs that have 15-year power purchase agreements locked in are commanding historic valuation premiums.

1. The Bloomberg Reality Check: The Gigawatt Deficit

To understand the sheer magnitude of the AI energy infrastructure 2026 opportunity, we must look at the hard data recently reported by major financial institutions. According to comprehensive industry analyses highlighted by Reuters Energy Correspondents, the global demand for data center power is projected to double, and in some regions triple, by the end of the decade.

Utility executives are currently rejecting connection requests from tech giants because the regional grids simply cannot physically handle the gigawatt loads required. We are witnessing a paradigm where the growth of AI is completely tethered to the production of base-load power. Solar and wind—while politically popular—are intermittent and entirely incapable of providing the 24/7, ultra-reliable 99.999% uptime that hyper-scale data centers demand.

This bottleneck has created the most lucrative asymmetrical investment opportunity of the decade. By allocating capital away from overvalued software companies and into the heavy, unglamorous world of physical energy assets, high-net-worth investors can secure massive yield and capital appreciation. Here are the three proven strategies being executed by the ultra-wealthy today.

2. Proven Strategy 1: The Nuclear Renaissance & SMRs

The most violent institutional rotation in the AI energy infrastructure 2026 thesis is the rapid pivot back to nuclear energy. Tech behemoths like Microsoft, Amazon, and Google have explicitly stated that their carbon-neutral pledges combined with their massive energy needs can only be solved by one mathematical equation: Nuclear power.

We have already seen unprecedented moves, such as tech companies directly purchasing nuclear power plants or signing 20-year Power Purchase Agreements (PPAs) at significant premiums to secure exclusive rights to a reactor’s output. For the sophisticated investor, there are two primary vectors to play this renaissance:

- Physical Uranium & Miners: Nuclear reactors require fuel. After a decade-long bear market post-Fukushima, the global supply of raw Uranium (U3O8) is in a severe structural deficit. Institutions are buying physical uranium trusts and top-tier miners (in tier-1 jurisdictions like Canada and the US), betting that the inelastic demand from existing and new reactors will drive commodity prices significantly higher.

- Small Modular Reactors (SMRs): Instead of taking 15 years and $20 billion to build a traditional massive nuclear plant, the future lies in SMRs. These are factory-built, smaller reactors that can be deployed directly on-site at a data center campus. Publicly traded companies designing and licensing this technology are highly speculative but represent the ultimate venture-style bet on the future of AI power.

3. Proven Strategy 2: Grid Modernization & Commodities

Even if we generate the power, we must transport it. The US electrical grid requires an estimated $2 trillion overhaul to handle the impending load from AI and the broader electrification of the economy (EVs, heat pumps). This leads us to the second pillar of the AI energy infrastructure 2026 thesis: the unglamorous physical materials required to build the grid.

You cannot build a data center, a nuclear plant, or a high-voltage transmission line without one critical element: Copper. According to the International Energy Agency (IEA), the world is facing a devastating shortfall of copper by the end of the decade. Discoveries of new copper mines have plummeted, and it takes an average of 15 years to bring a new mine from discovery to production.

Institutional investors are heavily allocating to copper miners, transformer manufacturers, and specialized industrial electrical equipment companies (like cooling systems and switchgears). These legacy industrial companies are experiencing massive earnings multiples expansion because they are the literal “pick and shovel” providers to the AI gold rush.

4. Proven Strategy 3: Power-Secured Real Estate (REITs)

The third strategy exists at the intersection of commercial real estate and technology. In the traditional commercial real estate market, location was everything. In the AI energy infrastructure 2026 market, power availability is everything.

The “Power-Secured” Premium

A barren plot of land in the Midwest is virtually worthless. However, if a real estate developer has spent five years navigating local zoning laws and has a legally binding agreement with the regional utility providing guaranteed access to 500 Megawatts of power, that plot of land instantly becomes worth tens of millions of dollars. Tech companies are desperately bidding up any real estate that already has power locked in.

High-net-worth investors access this premium through highly specialized Data Center Real Estate Investment Trusts (REITs) or through private equity infrastructure funds. These entities own the physical shell of the building, manage the massive industrial cooling systems, and lease the powered space to the hyperscalers on 15-to-20-year ironclad contracts. It provides equity-like growth with bond-like, inflation-protected yield.

5. The Institutional Pivot: Moving Beyond Public Tech

If your portfolio is solely heavily concentrated in the Nasdaq 100, you are taking on immense valuation risk while entirely missing the physical reality of the market. As an essential part of robust investing, true wealth preservation requires recognizing when a macro narrative transitions from software to hardware, and ultimately, to commodities and infrastructure.

The AI energy infrastructure 2026 supercycle is not a fad; it is a required physical build-out to support the next era of human technological advancement. By shifting capital into nuclear energy plays, grid modernization industrials, and power-secured real estate, investors can position themselves in the exact chokepoints where the world’s largest companies are forced to spend trillions of dollars.

Interactive: Infrastructure Alpha Simulator

See the mathematical impact of pivoting a portion of your portfolio away from pure Tech equities and into the AI energy infrastructure 2026 supercycle (Uranium, Copper, Grid Private Equity).

Shifting capital from broad equities into Energy/Grid Infrastructure.

Estimated annual “Alpha” (excess return) of infrastructure assets over standard S&P 500 returns due to structural supply deficits.

Macroeconomic & Investment Disclaimer

The information provided in this article regarding the AI energy infrastructure 2026 supercycle is for educational and analytical purposes only. It does not constitute professional financial, investment, or legal advice. Investments in physical commodities (Uranium, Copper), early-stage technologies (SMRs), and specialized REITs carry extremely high volatility, significant principal risk, potential illiquidity, and geopolitical vulnerability. The interactive “Alpha Simulator” assumes a hypothetical 8% base market return and is purely illustrative; it does not guarantee future performance. FinanceWise is not a registered investment advisor. You must consult with a certified fiduciary (CFP®) or institutional wealth manager before altering your asset allocation.

References & Citations

- Reuters Energy Reporting. Data center electricity demand forecasts and grid limitations. Available at Reuters.com.

- International Energy Agency (IEA). “Electricity 2024 – Analysis and forecast to 2026” and global copper supply deficit reports.