Direct Indexing vs ETFs: The 2026 Strategy for 2% Tax Alpha

Retail investors praise the simplicity of buying standard S&P 500 index funds. Institutional family offices, however, recognize that the standard ETF structure destroys a massive mathematical advantage: component-level tax-loss harvesting. Here is how the ultra-wealthy generate “Tax Alpha” out of thin air.

Financial media has spent the last two decades drilling a singular mantra into the minds of the American public: Buy a low-cost S&P 500 ETF and do nothing. Vehicles like Vanguard’s VOO or State Street’s SPY are universally heralded as the ultimate democratization of wealth building. They are incredibly cheap, highly diversified, and historically robust. However, when we elevate the conversation from middle-class accumulation to high-net-worth preservation, a glaring structural flaw emerges. If you are a high earner holding standard ETFs in a fully taxable brokerage account, you are fundamentally losing the Direct Indexing vs ETFs debate, leaving hundreds of thousands of dollars on the table for the IRS.

To understand why the ultra-wealthy avoid standard index funds in taxable accounts, we must deconstruct the mechanics of institutional asset management. A family office does not merely seek market returns (Beta); it aggressively seeks tax-optimized outperformance (Tax Alpha). They achieve this not by picking individual winning stocks, but by deploying a highly sophisticated strategy known as Direct Indexing. By unpacking the index and holding the constituent shares directly, they unlock an algorithmic harvesting mechanism that essentially forces the federal government to subsidize their capital gains.

The Direct Indexing Advantage Matrix

1. Algorithmic Harvesting

Automatically sell individual losing stocks within the S&P 500 daily to bank permanent capital losses, legally offsetting gains from real estate or stock options.

2. Concentration Shield

If you receive massive RSUs from a tech employer (e.g., Apple or Google), direct indexing allows you to strip those specific stocks out of your index to prevent dangerous overexposure.

3. TCJA Expiration Prep

Build a massive reservoir of “carry-forward” tax losses today to shield your wealth when top marginal brackets revert to 39.6% after the 2026 TCJA sunset.

The Institutional Edge: Why ETFs Leak Wealth

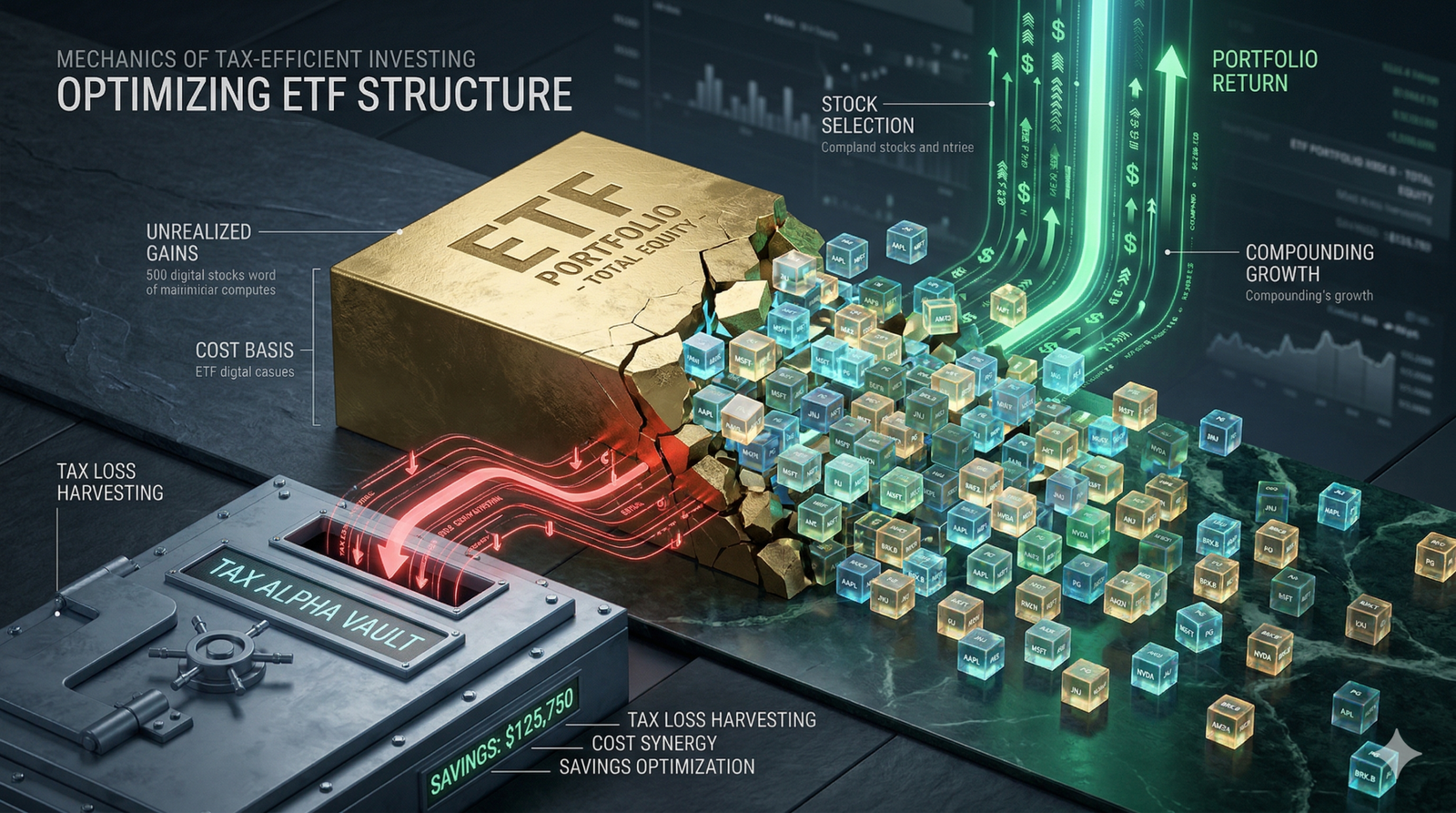

When you purchase a share of an ETF like SPY, you are buying a tightly wrapped, opaque basket of 500 stocks. You own a single ticker. From a taxation standpoint, this is highly restrictive. You only realize a capital gain or loss when you sell that single ticker.

Consider a hypothetical year where the broader S&P 500 index finishes up a spectacular +15%. As an ETF holder, you are thrilled. Your portfolio looks fantastic. But peel back the mathematical layers of that index. Even in a roaring bull market where the index is up 15%, the distribution of returns is wildly uneven. While technology giants might be up 40%, it is mathematically guaranteed that dozens, if not over a hundred, individual companies within that same index have suffered severe negative returns for the year.

Herein lies the critical flaw of the ETF structure for high earners: The losses of the underlying bad companies are trapped inside the wrapper. You cannot extract the loss of a failing telecom stock from your SPY ETF to offset the massive capital gains you triggered by selling your tech RSUs (Restricted Stock Units) or investment real estate. The losses simply net out against the gains internally, providing you with zero personal tax relief. In the core analysis of Direct Indexing vs ETFs, the ETF structure is a wealth-leaking straightjacket for anyone with a complex tax situation.

Deconstructing the Black Box: Algorithmic Harvesting

Direct Indexing shatters this straightjacket. Instead of buying one share of an ETF, you (or more accurately, a software algorithm operating your account) directly purchase fractional shares of the 500 individual companies that make up the index, weighting them identically to the benchmark. You have effectively cloned the S&P 500 in your personal brokerage account.

The Mechanism of Tax Alpha

Because you own the stocks directly, the algorithm constantly scans your portfolio for volatility. On a random Tuesday, if a specific banking stock drops 12% on bad earnings, the algorithm instantly sells that specific stock, realizing a hard, legal capital loss. It immediately reinvests that cash into a highly correlated competitor (maintaining your desired market exposure). At the end of the year, your portfolio tracks the S&P 500 perfectly, but you have legally banked tens of thousands of dollars in “harvested losses.”

These harvested losses are the holy grail of high-net-worth tax management. According to the IRS tax code, these capital losses can be used to offset your capital gains dollar-for-dollar. If you sell a rental property for a $100,000 profit, but your direct indexing algorithm harvested $60,000 in phantom stock losses throughout the year, you only pay taxes on $40,000. Furthermore, if your losses exceed your gains, up to $3,000 can be used to offset your ordinary income (like your W-2 salary), with the rest carrying forward indefinitely into future years[1]. This mathematical generation of net-new wealth through tax avoidance is what the industry defines as “Tax Alpha.” Historically, an aggressive direct indexing strategy can generate an additional 1.0% to 2.0% in annualized after-tax returns compared to a stagnant ETF.

Navigating the IRS Wash-Sale Barrier

At this point, you might wonder why an individual investor cannot simply do this manually. The primary barrier is the complexity of the federal tax code, specifically the Wash-Sale Rule.

Under the SEC and IRS guidelines on Wash Sales, you cannot sell a security at a loss and then buy a “substantially identical” security within 30 days before or after the sale. If you do, the IRS disallows the tax deduction. If you sell ExxonMobil at a loss, you cannot buy ExxonMobil back the next day. A human trader trying to harvest losses across 500 stocks would quickly run afoul of these rules, triggering massive tax penalties.

This is why evaluating Direct Indexing vs ETFs is largely an evaluation of software capability. Direct indexing platforms utilize sophisticated quantitative algorithms. When the system sells ExxonMobil at a loss, the algorithm automatically buys Chevron—a highly correlated proxy that keeps your energy sector exposure perfectly balanced without violating the wash-sale rule. After 31 days have passed, the algorithm can elegantly swap back if necessary. It is a level of frictionless, automated compliance that retail tools simply cannot replicate.

The 2026 Catalyst: Why Tax Alpha Matters Now

Direct indexing has always been mathematically superior for high-net-worth individuals, but a looming macroeconomic event is making it an absolute necessity. The Tax Cuts and Jobs Act (TCJA) of 2017 is scheduled to sunset at the end of 2025. This expiration will aggressively reshape the tax landscape for the American upper-middle class and wealthy brackets.

When the TCJA expires, top marginal income tax rates will revert from 37% back up to 39.6%. More importantly, the income thresholds defining the 15% and 20% long-term capital gains brackets will compress. In a high-tax environment, the value of a harvested loss increases exponentially. A $50,000 harvested loss saves you significantly more money when capital gains are taxed at 23.8% (including the Net Investment Income Tax) than it does at 15%. If you want to see exactly how your portfolio and salary will be hit by this incoming bracket creep, we strongly advise running your data through our 2026 Tax Calculator.

The core premise of the Direct Indexing vs ETFs debate in 2026 is defensive. You cannot control the federal reserve, and you cannot control the expiration of the TCJA. The only variable you can control is the location and structure of your assets. By establishing a direct indexing protocol today, you are actively building a reservoir of carry-forward tax losses that will serve as a shield against the heavy taxation expected in 2026 and beyond.

Visualizing the Fee vs. Alpha Spread

Understanding the net benefit after management fees.

Even after paying a higher management fee to the algorithm provider, the after-tax benefit far outweighs the cost for investors in the highest tax brackets.

The Verdict: Execution and Fee Drag

If direct indexing is mathematically superior, why isn’t everyone doing it? Historically, the barrier to entry was immense. Ten years ago, family offices needed a minimum of $5 million to $10 million in liquid assets to justify the transaction costs of maintaining 500 individual fractional shares. Today, zero-commission trading and algorithmic advancements have lowered the minimums at major brokerages (like Fidelity, Schwab, or Wealthfront) to as little as $5,000 to $100,000.

However, there is a catch. Direct indexing is not free. While an ETF like VOO charges a near-zero expense ratio of 0.03%, direct indexing platforms typically charge an AUM (Assets Under Management) fee ranging from 0.20% to 0.40%. Therefore, the final synthesis of the Direct Indexing vs ETFs equation requires a brutal assessment of your personal tax situation. If you are in a low tax bracket with no significant outside capital gains (like RSUs or real estate sales), the 0.30% fee drag will outweigh the tax benefits. You should stick to the ETF. But, if you are a high-income professional facing the 2026 tax cliff with significant taxable assets, failing to harvest your losses is an institutional-grade mistake.

The Tax Alpha Simulator

Calculate the net monetary benefit of Direct Indexing vs ETFs based on your expected capital gains tax rate.

Historical averages range between 1.0% and 2.0% annually, depending on market volatility.

Financial & Tax Disclaimer

The content provided on FinanceWise is for informational and educational purposes only and should not be construed as professional financial, investment, or tax advice. Generating “Tax Alpha” through direct indexing depends heavily on individual circumstances, market volatility, and continuous capital gains exposure. We do not guarantee any specific returns or tax outcomes. The Wash-Sale Rule is highly complex. Please consult a certified CPA and a fiduciary financial advisor to discuss the impact of the wash-sale rule and the TCJA expiration on your specific portfolio before executing these strategies.

References & Citations

- Internal Revenue Service (IRS). “Publication 550: Investment Income and Expenses (Including Capital Gains and Losses).” IRS.gov. Accessed 2026.

- U.S. Securities and Exchange Commission (SEC). “Wash Sales.” Investor.gov.