You just got your first paycheck of 2026, and something looks… different. Maybe you’re taking home $30 more per month. Or maybe $30 less. You stare at the “Federal Tax” line wondering: did something change, or did payroll mess up?

Here’s what happened: the IRS adjusted tax brackets and deductions for 2026 to account for inflation, and those changes hit your paycheck starting January 1st.[1] For some people, that means a small raise. For others, it means their withholding is now wrong and they’re headed for a surprise tax bill next April.

This isn’t just about numbers on a W-2 form. These changes affect how much money hits your bank account every two weeks, whether you’ll owe taxes or get a refund, and how you should adjust your budget for the year ahead.

As a personal finance writer who’s analyzed tax policy for years, I’ll break down exactly what changed, how it impacts your specific income level, and—most importantly—what you need to do about it before you file your 2026 taxes.

What Actually Changed in 2026?

The IRS makes inflation adjustments every year, but 2026 saw some of the largest increases in recent history due to persistent inflation in 2024-2025.[2] Here are the changes that matter most:

1. Tax Brackets Shifted Up (But Rates Stayed the Same)

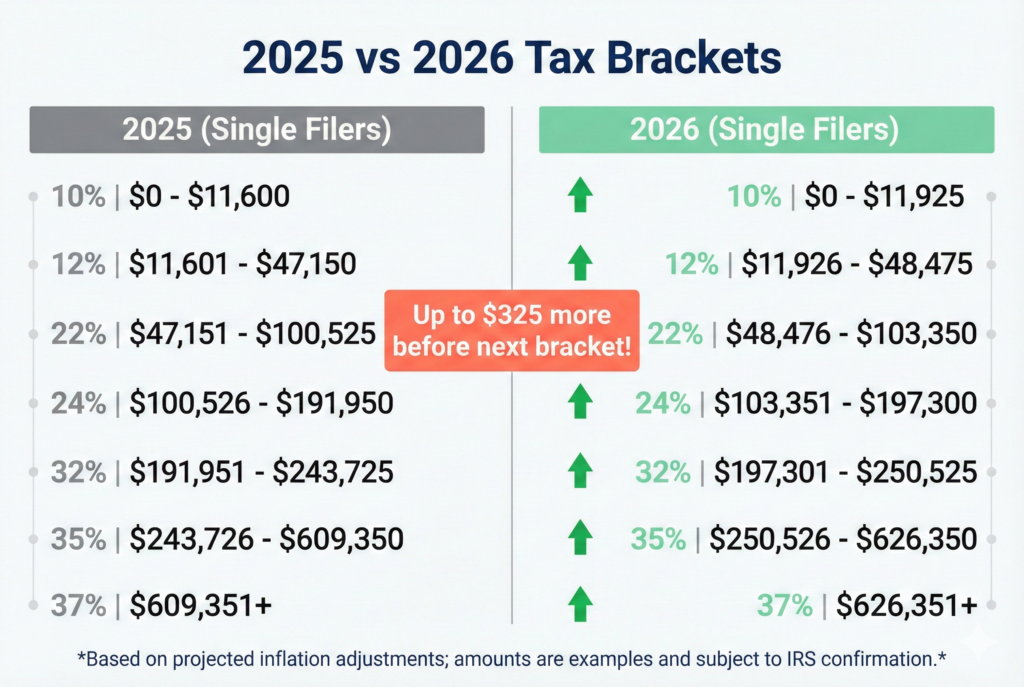

The seven federal tax rates didn’t change—they’re still 10%, 12%, 22%, 24%, 32%, 35%, and 37%. But the income thresholds for each bracket increased.

What this means in plain English: You can earn more money before jumping to the next tax bracket. That’s good news.

For single filers in 2026:[1]

- 10% bracket: Up to $11,925 (was $11,600 in 2025)

- 12% bracket: $11,926 to $48,475 (was $11,601 to $47,150)

- 22% bracket: $48,476 to $103,350 (was $47,151 to $100,525)

- 24% bracket: $103,351 to $197,300 (was $100,526 to $191,950)

- 32% bracket: $197,301 to $250,525 (was $191,951 to $243,725)

- 35% bracket: $250,526 to $626,350 (was $243,726 to $609,350)

- 37% bracket: Over $626,350 (was over $609,350)

For married filing jointly:[1]

- 10% bracket: Up to $23,850 (was $23,200)

- 12% bracket: $23,851 to $96,950 (was $23,201 to $94,300)

- 22% bracket: $96,951 to $206,700 (was $94,301 to $201,050)

- 24% bracket: $206,701 to $394,600 (was $201,051 to $383,900)

- 32% bracket: $394,601 to $501,050 (was $383,901 to $487,450)

- 35% bracket: $501,051 to $751,600 (was $487,451 to $731,200)

- 37% bracket: Over $751,600 (was over $731,200)

2. Standard Deduction Increased

This is the automatic deduction everyone gets before calculating taxable income.

2026 Standard Deductions:[1]

- Single filers: $15,000 (up from $14,600 in 2025)

- Married filing jointly: $30,000 (up from $29,200)

- Head of household: $22,500 (up from $21,900)

Real impact: If you’re single and earn $50,000, your taxable income drops from $35,400 (in 2025) to $35,000 (in 2026). That’s $400 less income getting taxed.

3. Earned Income Tax Credit (EITC) Expanded

The EITC helps low-to-moderate income workers, and the 2026 limits increased significantly.[3]

Maximum credit amounts for 2026:

- No children: $649 (was $632)

- One child: $4,213 (was $4,098)

- Two children: $6,960 (was $6,765)

- Three+ children: $7,830 (was $7,611)

Income phase-out limits (single filers):

- No children: $19,104 (was $18,591)

- One child: $49,084 (was $47,746)

- Two children: $55,768 (was $54,272)

- Three+ children: $59,328 (was $57,743)

If you’re a single parent earning $45,000 with one child, you could get back over $4,000 with EITC. That’s not pocket change.

4. Child Tax Credit Stayed the Same (But That’s a Problem)

Unlike almost everything else, the Child Tax Credit did NOT get an inflation adjustment. It’s still:

- $2,000 per child under 17

- Up to $1,700 refundable

My take: This is frustrating. While tax brackets adjusted for inflation, the credit that helps parents the most stayed frozen. A $2,000 credit in 2026 buys less than it did in 2020, yet Congress hasn’t updated it.[4]

5. Retirement Contribution Limits Increased

401(k), 403(b), and most 457 plans:[5]

- Employee contribution limit: $23,500 (up from $23,000)

- Catch-up contributions (age 50+): $7,500 (unchanged)

- Total employee + employer limit: $70,000 (up from $69,000)

IRA contributions:[5]

- Traditional and Roth IRA: $7,000 (up from $6,500)

- Catch-up (age 50+): $1,000 (unchanged)

What this means: You can shield more income from taxes by maxing out retirement accounts. If you were already contributing the 2025 max, increase your contributions to take full advantage.

How These Changes Affect Your Actual Paycheck

Let’s get specific. Here’s how different income levels are impacted:

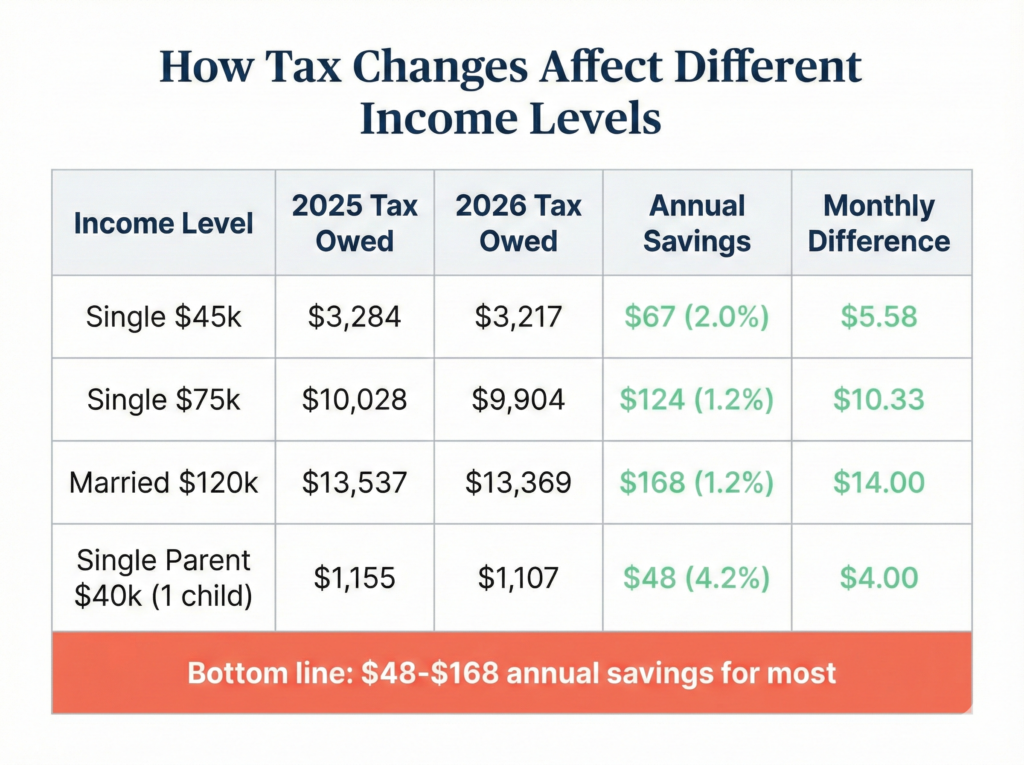

Example 1: Single, Earning $45,000

2025 taxes:

- Taxable income: $45,000 – $14,600 = $30,400

- Tax owed: ~$3,480

2026 taxes:

- Taxable income: $45,000 – $15,000 = $30,000

- Tax owed: ~$3,432

Savings: ~$48/year ($4/month)

The reality: You’ll barely notice. The standard deduction increase saves you about the cost of one streaming service per month.

Example 2: Single, Earning $75,000

2025 taxes:

- Taxable income: $75,000 – $14,600 = $60,400

- Tax owed: ~$9,574

2026 taxes:

- Taxable income: $75,000 – $15,000 = $60,000

- Tax owed: ~$9,486

Savings: ~$88/year ($7/month)

The reality: Still minimal savings. You’re getting an extra coffee per week.

Example 3: Married Filing Jointly, Earning $120,000

2025 taxes:

- Taxable income: $120,000 – $29,200 = $90,800

- Tax owed: ~$12,482

2026 taxes:

- Taxable income: $120,000 – $30,000 = $90,000

- Tax owed: ~$12,322

Savings: ~$160/year ($13/month)

The reality: A dual-income household sees slightly better savings, but it’s still less than a tank of gas per month.

Example 4: Single Parent, Earning $40,000, One Child

2025 taxes (before credits):

- Taxable income: $40,000 – $14,600 = $25,400

- Tax owed: ~$2,868

- Minus Child Tax Credit: -$2,000

- Minus EITC: -$3,995

- Refund: ~$3,127

2026 taxes (before credits):

- Taxable income: $40,000 – $15,000 = $25,000

- Tax owed: ~$2,820

- Minus Child Tax Credit: -$2,000

- Minus EITC: -$4,115

- Refund: ~$3,295

Difference: ~$168 larger refund

The reality: Working parents with lower incomes benefit most from the EITC expansion. That’s actually meaningful money.

My Honest Take: Is This Enough?

As someone who writes about personal finance for a living and watches tax policy closely, here’s what frustrates me about these 2026 changes:

The Good

Inflation adjustments prevent “bracket creep.” Without these changes, you’d effectively get a pay cut. If your salary increased 3% to keep pace with inflation but your tax bracket didn’t adjust, more of your income would get taxed at higher rates. These adjustments prevent that.

The EITC expansion actually helps people who need it. An extra $100-200 for a family earning $40,000 matters way more than it does for someone earning $150,000.

The Frustrating

These changes barely keep up with real inflation. According to the Bureau of Labor Statistics, inflation ran at 3.4% in 2024 and 2.8% in 2025.[6] The tax adjustments roughly match that, which means you’re treading water—not getting ahead.

The Child Tax Credit is frozen. A $2,000 credit in 2020 had more buying power than $2,000 in 2026. Families are effectively getting less help while costs for childcare, food, and education keep climbing.

These changes do almost nothing for middle-class earners. If you’re single making $60,000, you’re saving maybe $6/month. That doesn’t move the needle on student loans, rent, or building an emergency fund.

The Reality Check

Tax policy is supposed to help people build financial stability. These 2026 changes? They’re maintenance adjustments—necessary to prevent things from getting worse, but not sufficient to make things better.

If you’re waiting for tax changes to solve your money problems, you’ll be waiting a long time. The real move is controlling what you can: maxing out that higher 401(k) limit, claiming every credit you qualify for, and building your financial foundation regardless of what Washington does.

What You Need to Do Right Now

These tax changes are automatic—you don’t have to file anything special to benefit. But there are actions you should take:

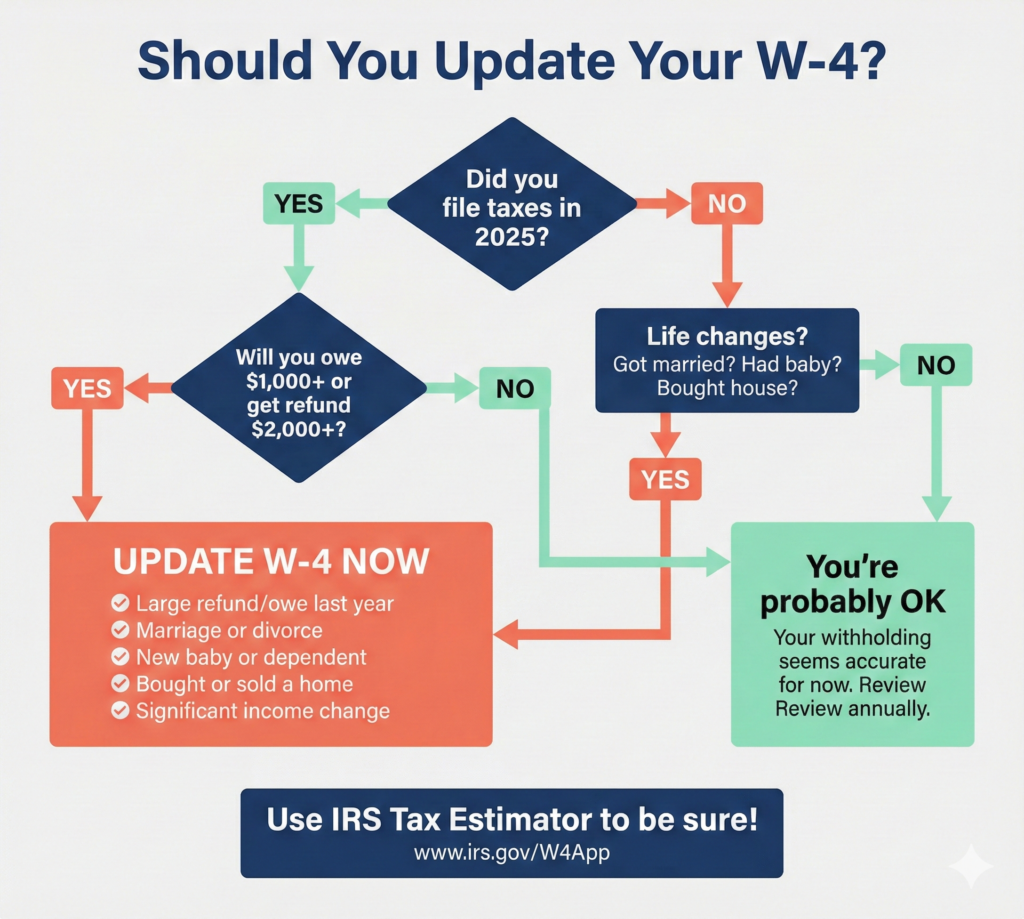

1. Check Your Withholding (Seriously, Do This)

Your employer’s payroll system should have automatically adjusted for 2026, but mistakes happen. Plus, if your life changed in 2025 (got married, had a kid, bought a house), your withholding might be wrong.

How to check:

- Go to the IRS Tax Withholding Estimator: irs.gov/W4App[7]

- Enter your 2025 tax return info

- Enter your current pay stub details

- See if you’re on track for a refund, owing taxes, or breaking even

Goal: Aim to owe or get refunded less than $500. Getting a big refund means you gave the IRS an interest-free loan all year.

2. Update Your W-4 If Needed

If the estimator says you’ll owe $1,000+ or get a refund over $2,000, update your W-4.

How to do it:

- Download the new W-4 form from IRS.gov

- Fill out Step 1 (personal info) and Step 5 (signature)

- Complete Step 2 only if you have multiple jobs

- Complete Step 3 if you claim dependents

- Complete Step 4 if you want extra withholding or have deductions

- Submit to your HR department

Note: The W-4 changed in 2020. Don’t use an old version.

3. Maximize Your Retirement Contributions

The 401(k) limit went up $500. If you were maxing out at $23,000, increase to $23,500.

Why this matters:

- Every dollar you contribute reduces your taxable income

- At the 22% bracket, contributing an extra $500 saves $110 in taxes

- That $500 grows tax-free for decades

How to do it: Log into your 401(k) account and increase your contribution percentage. Most plans let you change this anytime.

4. Plan for Tax Credits You Might Qualify For

Don’t leave money on the table. Check if you qualify for:

Earned Income Tax Credit (EITC):

- Single parent earning under $49,000 with one kid

- Married couple under $60,000 with two kids

- Single person under $19,000 with no kids

Child Tax Credit:

- $2,000 per child under 17

- Income phase-out starts at $200,000 (single) or $400,000 (married)

Lifetime Learning Credit:

- Up to $2,000 for college or job training courses

- You don’t have to be pursuing a degree

Saver’s Credit:

- Up to $1,000 ($2,000 married) for retirement contributions

- Only if you earn under $38,250 (single) or $76,500 (married)

5. Adjust Your Budget for the New Reality

If you got a small raise from these tax changes, great. But don’t count on it to fix your budget.

Better approach:

- Revisit your 50/30/20 budget with your actual take-home pay

- If you’re getting more per paycheck, redirect it to emergency savings or debt payoff

- If you’re getting less (because withholding adjusted), find the gap in your budget now—not in December

Common Mistakes People Make with Tax Changes

Mistake #1: Ignoring Withholding Until Tax Time

You file your taxes in April 2027 and owe $2,500. Surprise! You didn’t have enough withheld all year.

Fix it now: Check your withholding in February, not February of next year.

Mistake #2: Chasing a Big Refund

“I love getting $3,000 back every April!”

No. You just gave the government a $3,000 interest-free loan while you paid 18% interest on your credit card.

Better approach: Adjust withholding so you break even, then put that extra $250/month into a high-yield savings account earning 4-5%.

Mistake #3: Not Updating W-4 After Life Changes

Got married in 2025? Had a baby? Bought a house? Your W-4 from 2023 is now wrong.

Fix it: Life change = W-4 update. Every time.

Mistake #4: Forgetting About State Taxes

This article covered federal changes. Your state might have made changes too—or might not have. Don’t assume your state withholding is correct just because federal is.

Mistake #5: Missing the Retirement Contribution Deadline

You have until April 15, 2027 to max out your 2026 IRA contributions. But most people forget and miss out on thousands in tax savings.

Set a reminder: March 2027 to max out IRA if you haven’t already.

Looking Ahead: What Might Change in 2027?

Tax policy is always evolving. Here’s what might impact your taxes next year:

The 2017 Tax Cuts and Jobs Act (TCJA) expires at the end of 2025. Many provisions sunset, which could mean:[8]

- Lower standard deductions (back to ~$7,000 for singles)

- Different tax brackets

- Return of personal exemptions

- Changes to itemized deductions

However: Congress will likely extend or modify these provisions rather than let them all expire. Expect political fighting about this through 2025-2026.

What to watch:

- Any Build Back Better revival affecting child tax credits

- Potential changes to SALT (state and local tax) deduction cap

- Adjustments to capital gains rates

My prediction: Expect more of the same—incremental inflation adjustments with partisan gridlock preventing major reforms.

Your Action Plan: What to Do This Week

Tax changes are passive—they happen whether you pay attention or not. But your response shouldn’t be passive.

This week:

- Check your most recent pay stub and compare federal withholding to last year

- Go to IRS.gov/W4App and run the withholding estimator

- If you’re way off, submit a new W-4 to HR

This month:

- Increase your 401(k) contribution to account for the new $23,500 limit

- Set up a high-yield savings account if that $50-100/year in tax savings is hitting your checking account

- Review which tax credits you might qualify for in 2026

Before April 2027:

- Make sure you’ve claimed all credits and deductions

- Max out your IRA contribution if you can afford it

- File on time to avoid penalties

The 2026 tax changes won’t make you rich. They won’t solve your financial problems. But understanding them—and adjusting your withholding, contributions, and budget accordingly—puts you in control instead of leaving you surprised every paycheck or every April.

Sources

[1] Internal Revenue Service, “IRS provides tax inflation adjustments for tax year 2026,” IR-2025-220, November 2025, https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2026

[2] U.S. Bureau of Labor Statistics, “Consumer Price Index Summary,” January 2026, https://www.bls.gov/news.release/cpi.nr0.htm

[3] Internal Revenue Service, “Earned Income Tax Credit (EITC) – 2026 Income Limits and Maximum Credit Amounts,” accessed February 2026, https://www.irs.gov/credits-deductions/individuals/earned-income-tax-credit

[4] Tax Policy Center, “Child Tax Credit: A Brief History,” Urban Institute & Brookings Institution, 2025

[5] Internal Revenue Service, “401(k) limit increases to $23,500 for 2026, IRA limit rises to $7,000,” November 2025, https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2026

[6] U.S. Bureau of Labor Statistics, “12-month percentage change, Consumer Price Index,” data through January 2026

[7] Internal Revenue Service, “Tax Withholding Estimator,” https://www.irs.gov/individuals/tax-withholding-estimator

[8] Tax Foundation, “Options for Reforming America’s Tax Code 2.0,” June 2025, https://taxfoundation.org/research/all/federal/tax-reform-options/

Disclaimer: This article is for educational purposes only and does not constitute tax or financial advice. Tax laws are complex and change frequently. Consult with a qualified tax professional or financial advisor for personalized guidance based on your specific situation.

About the Author: The FinanceWise team is dedicated to making complex financial topics like taxes accessible and actionable for young adults. We believe understanding tax policy shouldn’t require a law degree—just clear explanations and honest analysis.