3 Reasons the Whole Life Insurance Trap Destroys Wealth

Every day, thousands of new parents and middle-class earners are sold expensive insurance policies disguised as “investments.” Discover the brutal math behind the industry’s biggest wealth killer.

Table of Contents

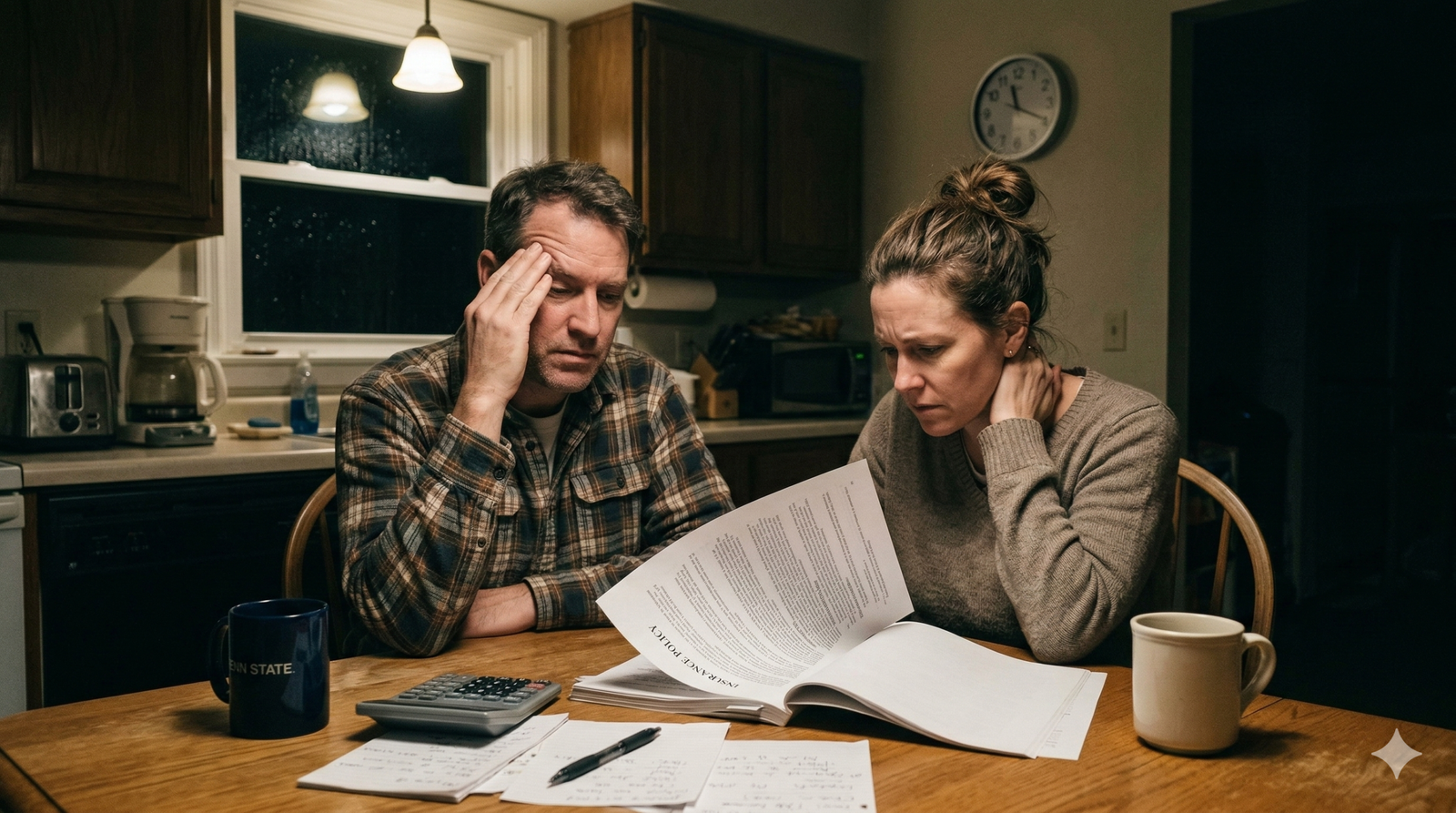

If you recently had a child, bought a house, or started a new career, you have likely received a call from an agent pitching you the Whole Life Insurance Trap—one of the most devastating financial mistakes a middle-class family can make.

The Mathematics Behind the Whole Life Insurance Trap

To understand why the whole life insurance trap is so dangerous, you must first understand the illusion of the “cash value.” Agents inaccurately compare whole life to “owning” a home, while term is “renting.” However, high fees and commissions mean your cash value stays at $0 for years.

According to the SEC’s Investor.gov guidelines, the heavy fees associated with permanent insurance can severely limit your long-term wealth compared to simple index funds.

Expert Insight: The Commission Motive

“The whole life insurance trap is sustained by an incentive structure that rewards salespeople for maximizing your monthly premium, often paying them up to 100% of your first year’s payments.”

Term Life: The Shield the Wealthy Actually Use

Life insurance is risk management, not an investment. You do not expect a return on car insurance. Term Life Insurance provides cheap, massive protection when you actually need it (during your working years).

The “Invest the Difference” Strategy

Real-World Impact: Two Families, 20 Years Later

Properly managing cash flow is key. Just as we discussed in our guide to escaping the credit card debt cycle, avoiding bad financial products requires ruthless mathematical discipline.

Do You Actually Need Permanent Coverage?

Single, No Dependents

No dependents? No life insurance needed. Invest in a Roth IRA instead.

Parents & Mortgage

Buy 20-30 year term for 10x-12x income. Protect your family cheaply.

Ultra-HNW ($25M+)

Only for estate tax liquidity. This is for the top 1%.

Action Steps: Escaping the Trap

- Never Cancel Without Replacement: Get your Term policy active before touching the old one.

- Shop for Term: Use an independent broker for the lowest 20-year rates.

- Request Cash Surrender: Take your surrender value and put it into an S&P 500 index fund.

Insurance, Investment & YMYL Disclaimer

The content provided on FinanceWise is for informational purposes only and should not be construed as professional insurance, legal, or tax advice. Cancelling an existing permanent life insurance policy can lead to significant financial loss (surrender charges) and may have tax implications. Furthermore, your ability to secure a new term policy depends on your current health status and age. Never cancel coverage before a replacement policy is in force. Always consult with a Certified Financial Planner (CFP®), a CPA, or a licensed insurance professional before making changes to your protection strategy.

The Wealth Building Simulator

Compare the whole life insurance trap vs. Term & Invest the difference.

1 thought on “3 Reasons the Whole Life Insurance Trap Destroys Wealth”

Comments are closed.